This guide draws on publicly available regulatory frameworks, permit guidance, and agency documentation from FEMA, Florida DEP, Florida FWC, the Jupiter Inlet District, the Town of Jupiter, and Palm Beach County. It reflects our operational experience advising waterfront buyers and sellers in northern Palm Beach County and should not be relied upon as legal, tax, insurance, or engineering advice. All figures cited are standard regulatory reference points; project-specific conditions vary, and licensed professionals should verify any figure before it informs a purchasing decision.

The Four-System Framework

Waterfront due diligence in Jupiter operates as an interconnected system rather than a sequential checklist. Elevation determines insurance cost. Dock geometry depends on riparian lines. Preserve designations govern in-water work. Insurance pricing reflects all three. The practical value of understanding these connections is that it changes what you ask, in what order, and of whom, before you draft an offer.

FEMA's Risk Rating 2.0 prices flood insurance using property-specific inputs: first-floor height, distance to water, foundation type, rebuild cost. Two adjacent homes on the same block can carry materially different premiums. Start with the Flood Map panel and Elevation Certificate before evaluating any other factor.

Florida riparian rights cover ingress, egress, boating, and fishing, but below mean high-water the State generally holds Sovereign Submerged Lands in trust. Most private dock structures require both regulatory and proprietary State authorization. Under standard DEP ERP guidance, most structures must be set back 25 feet inside riparian lines, with 10 feet for qualifying marginal dock configurations. Project-specific conditions vary, and confirmation with DEP or a qualified marine contractor is essential before committing to any dock design.

The Loxahatchee River-Lake Worth Creek Aquatic Preserve and the federally designated Wild & Scenic Northwest Fork are not incidental designations. They are the reason Jupiter's water remains extraordinary. They also govern in-water work, adding regulatory review and constraining certain activities. Understanding the framework is part of responsible ownership here.

Florida's insurance market continues to evolve. Get at least two quotes (Citizens if eligible, plus one private carrier) and model the five-year cost differential against the home's elevation and flood zone. Pair windstorm and dedicated flood coverage via NFIP or a private form priced under Risk Rating 2.0.

Elevation, Freeboard & Flood Zones: The Baseline

Start with three documents: the FEMA Flood Map panel for the parcel, the latest Elevation Certificate, and the Town's floodplain standards. These are not formalities. They determine your insurance premium, your renovation budget, and your ability to modify the structure over time. FEMA's Risk Rating 2.0 prices flood insurance using property-specific factors rather than zone categories alone. Two adjacent homes can carry different premiums. Flood maps remain your spatial and regulatory guide; Risk Rating 2.0 is the pricing lens. Use both.

In the Town of Jupiter, new construction typically must elevate to ASCE 24 or Base Flood Elevation + 1.5 feet, whichever is higher. This is a local code safeguard that compounds value over time. At the county level, flood ordinances embed freeboard standards and "substantial improvement" thresholds that apply to additions as much as to new builds. A renovation exceeding 50% of assessed value triggers full compliance with current flood standards, a factor that affects renovation budgets materially on older homes.

Practical Rhythm for Elevation Due Diligence

Riparian Rights, Docks & the 25-Foot Logic

In Florida, riparian rights run with lands abutting navigable waters (ingress, egress, boating, bathing, fishing), but they are not a deed to the bottom. Below the mean high-water line, the State generally holds Sovereign Submerged Lands in trust. Most private structures require both regulatory and proprietary State authorization.

For many single-family docks, Florida offers a streamlined path: ERP Self-Certification for qualifying projects. Otherwise, a Letter of Consent or lease governs use of Sovereign Submerged Lands. Under standard DEP guidance, most structures must be set back 25 feet inside riparian lines, with 10 feet for qualifying marginal docks. Limited exceptions and neighbor waivers are available in specific circumstances, and project-specific conditions always apply. Plan your boatlift and mooring piles within this geometry before engaging a designer.

The geometry comes before the design. Buyers who commit to a property and then discover the dock geometry cannot accommodate their vessel lose either the property or the boat. Plot riparian lines on a current survey before engaging a dock designer, and confirm the depth at mean low water before sizing a lift. These are pre-offer questions, not post-closing discoveries.

Buyer Checklist: Riparian Rights & Dock Permitting

Aquatic Preserves, Wild & Scenic Waters & Why They Matter

Jupiter's waters are extraordinary because they are protected. The Loxahatchee River-Lake Worth Creek Aquatic Preserve frames much of the daily boating life here, while the Northwest Fork carries a federal designation as a National Wild & Scenic River, one of Florida's very few. These designations are not regulatory footnotes. They are the reason the water looks the way it does, and the reason it will continue to look that way. They also govern what in-water work is permissible and add regulatory review to projects that might be straightforward elsewhere in South Florida.

Local management is substantive. The Jupiter Inlet District coordinates navigation, access, signage, and river management, balancing recreational use with resource protection across the Central Embayment and river forks. Understanding the regulatory framework before purchase eliminates the most common source of friction in long-term ownership on these waters.

The constraint and the value are the same thing. Aquatic preserve and Wild & Scenic designations prioritize habitat, water quality, seagrasses, mangroves, and public enjoyment. For in-water work (seawall replacement, dock extensions, mooring modifications) they add regulatory review and constrain certain activities. They also ensure that the views, water quality, and ecology that make this address compelling cannot be developed away by a future neighbor or an adjacent landowner. Understanding the regulatory framework as a permanent feature of the asset, not an inconvenience to be navigated, is the difference between a frustrated owner and one who made the purchase with full information.

Wake Zones, Manatees & Seasonal Rhythm

Speed rules shift with the season to protect wildlife and shorelines. On the lower Loxahatchee, expect Slow Speed, Minimum Wake with signage shifting between winter (November 15 through March 31, channel exempt) and summer (within 300 feet of shore) patterns. In February 2025, FWC approved an additional year-round Slow Speed, Minimum Wake zone north of Cato's Bridge in Jupiter Narrows, with enforcement initially emphasizing education over citation.

These zones are the reason a June evening on the river is genuinely quiet. They protect seawalls, shorelines, and wildlife, and the managed pace of boat traffic is a primary reason buyers who have boated elsewhere in South Florida consistently cite the river as a deciding factor. That quietness is deliberate and structural - not a restriction on use, but a feature of the address.

Insurance: Model the Cost Before You Offer

Under Risk Rating 2.0, elevation relative to Base Flood Elevation is the single most controllable variable in your flood premium. The practical question for any specific property is how much of the premium is addressable through documentation (elevation certificates, wind mitigation) versus fixed by geography and construction type. A property elevated well above BFE, with a documented Elevation Certificate, reinforced roof, and hurricane-rated openings, occupies a materially different insurance tier than a comparable footprint built to minimum code. That difference compounds over years of ownership and is directly reflected in resale positioning.

Florida's carrier landscape continues to evolve. Citizens Property Insurance moves eligible policies to private carriers through depopulation programs; portfolio mix and pricing shift year by year. For buyers at this level, the relevant exercise is not confirming that insurance is available. It is modeling what it costs at a specific address, under multiple carrier scenarios, over a five-year holding period. That model belongs in your offer analysis, not your closing checklist.

Insurance Due Diligence Before Close

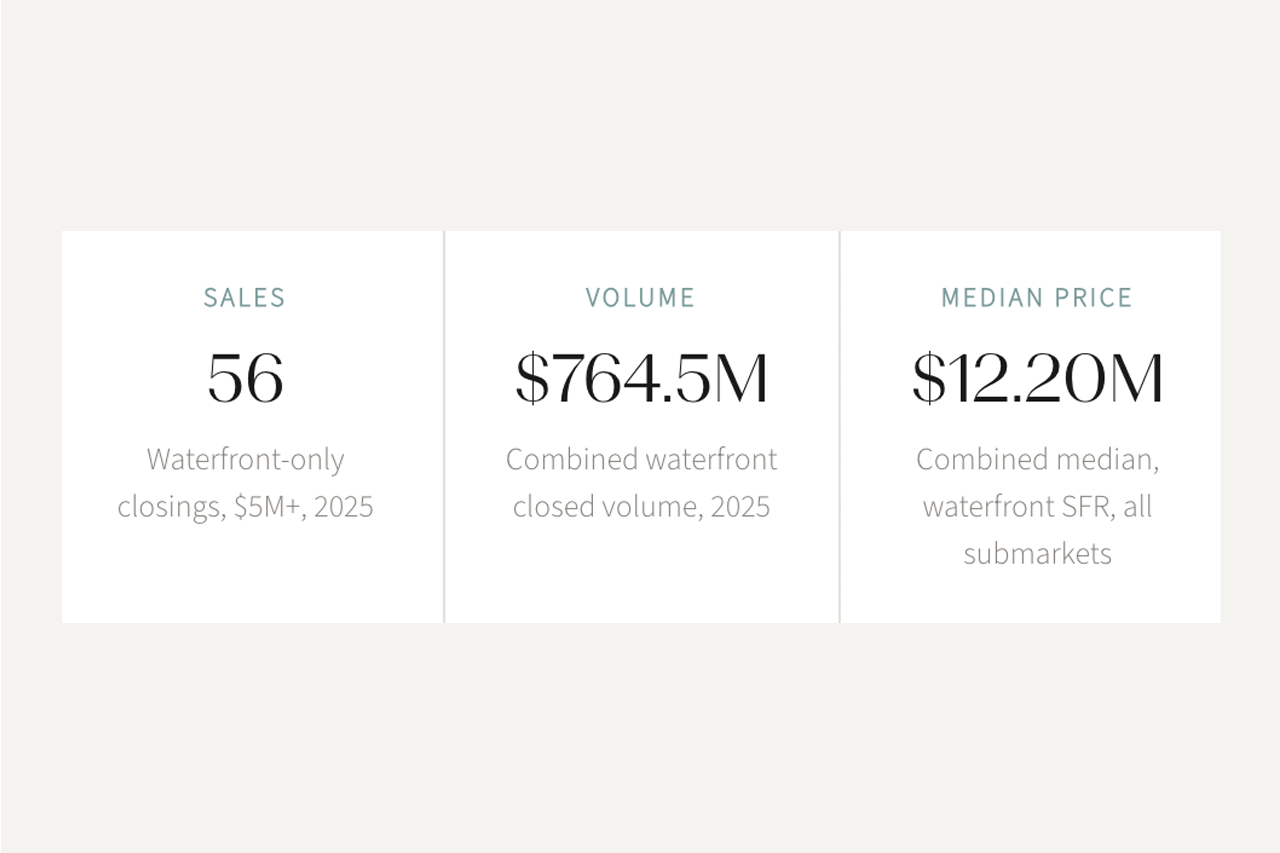

What Value Really Means on the Water

Jupiter's waterfront supply is permanently constrained by aquatic preserve boundaries, floodplain standards, and riparian permitting complexity. Every regulatory layer that adds friction to new development or in-water modification protects the scarcity value of existing inventory. This is the core investment thesis for waterfront here, and it is worth understanding precisely because the same constraints that protect value also define what you can and cannot do with the property after closing.

An inlet-side home with depth for a larger vessel may be irreplaceable to one buyer; a riverfront property with native shoreline and unobstructed western exposure may be worth more to the next owner. Because supply is constrained by aquatic preserve boundaries and navigable water frontage, the north county market rewards proportion, elevation, and functional dock geometry over time. The preserve designations that constrain in-water construction are the same designations that protect the ecology. The wake zones that limit boat speed are the reason the river is worth living on. The elevation requirements that add cost to new construction are the same standards that separate resilient assets from vulnerable ones.

Bottom Line

Jupiter's waterfront market is one of the most defensible in South Florida because it is constrained. The aquatic preserve designations, floodplain standards, wake zone management, and riparian permitting framework all protect scarcity by making the water harder to develop and harder to degrade. Due diligence at this level is not about finding reasons not to buy. It is about arriving at a price and a structure that reflect what you actually own - accomplished through three documents, two insurance quotes, one current survey with riparian lines plotted, and a conversation with the building department before you design anything.

For buyers planning new construction or major renovation: Confirm the BFE and local freeboard requirement first. Calculate whether your renovation scope crosses the 50% substantial-improvement threshold before agreeing on price. This single calculation can shift your effective purchase cost by hundreds of thousands of dollars and should be completed before offer, not during inspection.

For buyers with vessels requiring dock or lift work: Plot riparian lines on a current survey with the 25-foot setback geometry marked, and confirm water depth at mean low water at the proposed lift location. These two measurements define whether the property works for your vessel. Defer them to the inspection period and you negotiate from sunk cost, not information.

For all waterfront buyers at $5M+: Model your five-year insurance cost under at least two carrier scenarios before offer, using the property's actual elevation and flood zone designation. Under Risk Rating 2.0, elevation is the most controllable variable in your premium, and the difference between well-documented and undocumented properties compounds over a holding period.

Palm Beach Luxury at Compass advises ultra-high-net-worth buyers and sellers across Palm Beach County's principal luxury submarkets. This guide reflects our operational experience in northern Palm Beach County waterfront transactions and should not be relied upon as legal, tax, insurance, or engineering advice.

The guide draws on publicly available regulatory documents, permit frameworks, and agency guidance from FEMA, Florida DEP, Florida FWC, the Jupiter Inlet District, and the Florida Bar. Riparian setback figures (25 ft standard / 10 ft marginal) reflect standard DEP ERP guidance; project-specific conditions vary and should be confirmed with DEP or a qualified marine contractor. Insurance observations reflect the general structure of Florida's market as of early 2025; premiums vary materially by property, carrier, and coverage tier. Buyers should verify all figures with licensed professionals before making purchasing decisions.

FEMA, Risk Rating 2.0 methodology and pricing approach: fema.gov/flood-insurance/risk-rating

Town of Jupiter, Flood Zones and Insurance Information (mapping tools): jupiter.fl.us/377/Flood-Zones-Insurance-Information

Florida DEP, Dock permitting guide (25-foot setback / 10-foot marginal, waivers): floridadep.gov, ERP Quick Guide (PDF)

Florida Statutes, Mean high-water and boundaries: Florida Statutes S. 177.28

Florida Bar Journal, Sovereign submerged lands and riparian rights: floridabar.org, Murky Bottoms

Florida DEP, Loxahatchee River-Lake Worth Creek Aquatic Preserve Management Plan: floridadep.gov, Loxahatchee Management Plan

FWC, 2025 Jupiter Narrows year-round slow-speed zone near Cato's Bridge: myfwc.com, Jupiter Narrows