What Matters

Evaluate flood zone, elevation, building envelope, drainage, and functional water access before price. These variables determine cost of carry and future buyer depth more reliably than finishes or renovation specifications.

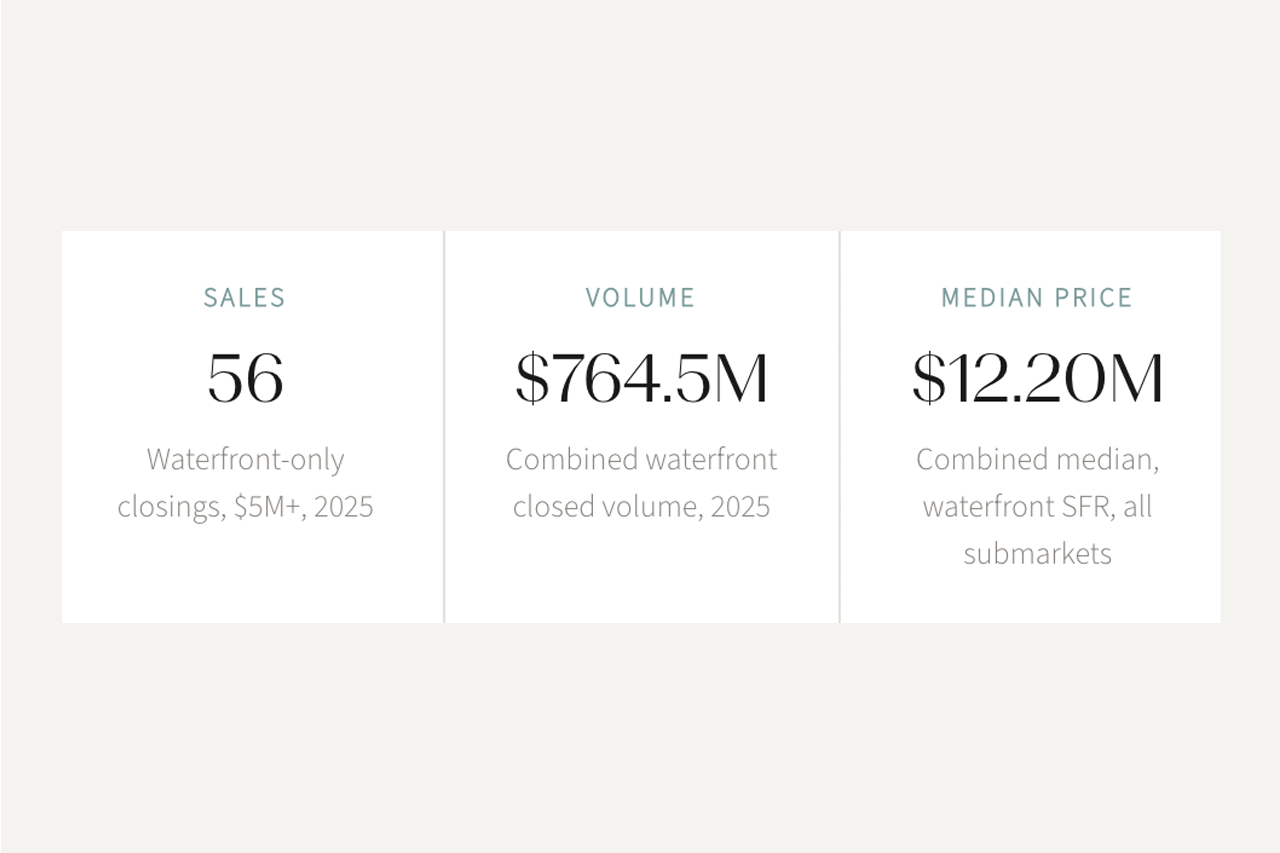

Why Now

Private carrier participation in Florida has stabilized selectively as of early 2026. Documented mitigation, resilient construction, and complete files command better terms and access to a broader pool of qualified buyers at $5M and above.

For Whom

Buyers and sellers at $5M and above in Palm Beach County, and the advisors, family offices, and lenders assessing risk, liquidity, and capital deployment for waterfront assets.

The Short Version

Market Context: Insurability Is the New Rate

Palm Beach luxury real estate has normalized from the pace of 2021 and 2022, but the upper tiers are now defined by insurability and function rather than momentum alone. Inventory above $5M has widened from 2023 lows, while absorption at $10M and above remains divided: turnkey, resilient waterfront moves; assets with unresolved compliance exposure or documentation gaps linger. Mortgage rates remain meaningfully above post-pandemic levels. More consequentially, insurance underwriting has become the qualifying filter that rate charts used to be.

Private carriers have returned to Florida on a selective basis, and buyers who present well-documented mitigation - impact-rated openings, sealed roof decks, elevated mechanicals - are quoting faster and often at lower cost than those without. On the water, not all frontage trades equally. Jupiter waterfront homes with protected water and consistent navigational draft attract deeper buyer pools than exposure-prone parcels near inlet turbulence or low bridge clearances. Well-positioned coastal property with functional docks and quiet water commands a measurable premium over otherwise comparable assets where daily use is constrained.

The closing that fails in this segment almost always fails on documentation that was discoverable before the offer was written. An outdated elevation certificate, a missing wind-mitigation report, or an unpriced seawall remediation creates a renegotiation event that compresses seller proceeds and extends timelines. The remedy is sequencing: assemble the file before the first showing, not during escrow.

What We Look For: Underwriting the Asset Before Pricing It

Every property we advise on - buy side or sell side - receives a structured assessment of quality signals and risk signals before a price recommendation is made. Finishes are secondary. The variables below are primary.

On-Market and Off-Market: How Each Lane Works

On Market

For on-market properties, request a digital diligence room containing the elevation certificate, wind-mitigation report, roof letter, survey, and seawall documentation at the outset. Clean files price tighter, close faster, and create less renegotiation surface. When the documentation package is complete, the only variables remaining are price and terms - and that is exactly where you want the conversation to be.

Off Market

For off-market opportunities, secure a time-bound preliminary indication with inspection access, and obtain proof of funds alongside insurance pre-quotes before any terms discussion begins. Off-market transactions at this level clear only when pricing respects land value, replacement cost, and time horizon, and when both parties are negotiating from verified information rather than assumption. Arriving with insurance already resolved is the most credible signal of seriousness a buyer can deliver.

For Buyers: The Risk-First Process

Approach the search like an underwriter. Before responding to the view, validate FEMA zone, base flood elevation, wave-action lines, and topography. Confirm impact-rated openings, roof system, and drainage. Treat water access as a risk variable: bridge clearances, inlet behavior, and wake exposure shape daily use and future buyer depth in ways that are not recoverable after closing. The checklist below covers the full diligence scope. Several items require licensed specialists; our role is knowing what to flag and in what sequence.

Run homeowners and flood quotes before the offer. Model NFIP versus private flood options, deductible structures, and available mitigation credits through current wind-mitigation and roof documentation. Engage a marine engineer to assess the seawall, tie-backs, and dock. At $5M to $10M and above, these line items often drive the acquisition decision more than any finish or renovation specification - and the only way to know which situation you are in is to price them before the offer is written.

Buyer Diligence: Domicile, Homestead and Acquisition

Where documentation gaps exist - non-rated doors, an unsealed roof deck, aging mechanicals - convert them into price or term improvements: credits, seller-funded upgrades, or escrow holdbacks tied to a defined scope with a licensed contractor. A clean offer with compressed contingencies frequently outperforms a higher number with unresolved diligence exposure.

For Sellers: Positioning Starts with Insurability

Bottom Line

The waterfront market at $5M and above is now segmented by insurability, not location alone. Properties that transact cleanly are those where elevation, envelope, and water access were evaluated before anyone negotiated price. Properties that linger are those where those variables were left for the other party to discover. Every documentation gap converts into leverage for whoever finds it first - and at this price tier, that leverage reshapes outcomes by hundreds of thousands of dollars.

For buyers at $5M and above: Run the risk process before the offer, not during diligence. Confirm FEMA zone and elevation, obtain HO and flood quotes, and engage a marine engineer on seawall and dock condition. A buyer who arrives with insurance resolved and contingencies compressed wins against a higher offer that still has weeks of open discovery ahead. The documentation you build in diligence is the leverage that controls the negotiation.

For sellers preparing to list waterfront: The preparation window is before photos, not before closing. Commission a fresh wind-mitigation report, remedy non-rated openings, assemble the elevation certificate and permit record, and document current insurance premiums. The seller who delivers a complete diligence room at first showing eliminates the renegotiation surface before it forms.

For advisors assessing waterfront risk and liquidity: The segmentation of this market is now primarily an insurance story. Evaluate waterfront assets by elevation, envelope quality, and documentation completeness before assessing any location premium. A well-documented property with current mitigation credits and clean files will clear at tighter spreads than a trophy address with unresolved compliance exposure. The gap between those two outcomes is widening.

This article is informational and does not constitute legal, tax, or insurance advice. Consult qualified professionals before making any decision. Market observations reflect Palm Beach County waterfront activity at the $5M and above tier as of early 2026. Insurance market conditions and carrier participation change frequently; premium estimates and coverage availability should be verified with a licensed Florida surplus lines or admitted broker. Equal Housing Opportunity.

Flood and FEMA: FEMA Flood Map Service Center: msc.fema.gov. NFIP Overview: fema.gov/flood-insurance.

Resilience Standards: IBHS FORTIFIED Home Program: fortifiedhome.org.

Florida Insurance Regulation: Florida Office of Insurance Regulation: floir.com.

Local Resources: Palm Beach County Flood Zone Resources: discover.pbcgov.org/publicsafety/dem/Pages/Flood-Zone.aspx.