The analysis covers 599 closed residential sales above $500,000 at Admirals Cove, Jupiter, FL from 2015 through 2025, sourced from BeachesMLS and extracted February 2026. For each transaction we track sale price, price per square foot, closing year, and price tier, then segment by calendar year and four analytical phases defined by the mechanism of appreciation. The result is a complete decade-long record of how every tier of the market moved, in sequence, and what that sequence means for the community’s pricing today.

Ten years of continuous appreciation, with the 2022 inflection as the sharpest single-year repricing in the community’s recorded history (+46.3% YoY). The 2017 pause is the only year in the dataset where $/SF declined; in retrospect it was the market consolidating before its longest sustained run.

Average $/SF calculated as transaction-level mean across all closed sales in each calendar year. 2015: n=32. 2016: n=38. 2017: n=36. 2018: n=41. 2019: n=64. 2020: n=88. 2021: n=89. 2022: n=45. 2023: n=65. 2024: n=46. 2025: n=50. Annotated events verified against MLS source data.

Phase I: Baseline Drift (2015–2018)

The four-year baseline tells a quieter story than most people expect. Admirals Cove in 2015 was already an established waterfront community: not a value play, not a distressed market, but a mature gated enclave trading at reasonable luxury premiums. The $452/SF average that year was, in absolute terms, a fair price for what the community offered. What it was not was a price that reflected what the community would become.

The 2016 and 2017 years traced a gentle drift: $490/SF, then back to $470/SF. A -4.1% dip in 2017 is notable because it is the only year in the dataset that saw $/SF decline. At the time it read as consolidation. In retrospect it was the market pausing before a sustained run that has not reversed since. Volume in this period averaged 37 sales per year: steady, unspectacular, characteristic of a community that attracted committed buyers without the urgency that would arrive in 2019.

The signal that something was shifting came in 2018: $/SF jumped 18.8% to $558, the largest single-year increase on record until 2021. Volume also climbed to 41 sales and the $5M+ tier doubled from five homes in 2017 to seven. The buyers arriving in 2018 were paying meaningfully more per square foot than their predecessors and they were writing larger checks. The baseline was ending.

Phase II: The Velocity Surge (2019–2020)

If 2018 was the signal, 2019 was the eruption. Sales volume jumped from 41 to 64, a 56% increase in a single year. Total volume crossed $196 million, more than double the 2015 figure. The community was absorbing demand at a pace it had not seen since its founding years. But the more consequential 2019 event was not the volume: it was September, when 490 Mariner Drive closed at $10.5 million. It was the first transaction in Admirals Cove history to cross the $10 million threshold. The $10M+ tier was no longer hypothetical.

Then came 2020. The conventional expectation, that a global pandemic would pause the luxury real estate market, proved incorrect almost immediately. After a brief nine-sale first quarter that reflected early lockdown caution, Admirals Cove processed 20 closings in the second quarter, 30 in the third, and 29 in the fourth. The annual total reached 88 sales, a 37.5% increase over 2019’s already-elevated pace. The community was running at more than twice its 2015–2018 annual average. Total volume crossed $300 million for the first time.

What is notable about the 2019–2020 surge is that it was primarily a volume event, not yet a price event. $/SF moved from $571 to $631, a 10.5% increase, meaningful but not dramatic. The market was absorbing demand through velocity, processing buyers as fast as they arrived. The pricing reckoning would come later.

2019–2020 was a volume event. 2022 was a price event. The two mechanisms of appreciation operated in sequence, not simultaneously. When volume dropped by half in 2022, $/SF accelerated its fastest-ever annual gain.

Left axis: annual closed sales count. Right axis: average $/SF. The inverse relationship between volume and $/SF growth in 2022 is the clearest illustration of the market’s shift from velocity-driven to value-driven appreciation.

Phase III: The Bridge Year (2021)

2021 was where velocity and value first overlapped. Volume held near 2020 levels, 89 sales, but $/SF made its first major jump: from $631 to $775, a 22.8% increase. The market was simultaneously running at high pace and repricing aggressively. Both conditions would prove unsustainable at the same time, but together they produced the community’s most concentrated period of appreciation.

The defining transaction of 2021 was 176 Spyglass Lane in June: $24 million, 17,885 SF of living area, 368 feet of waterfrontage on a 63,832 SF lot. It was the new community ceiling, more than twice the 2019 record of $10.5 million (2.3×), and it established a price level that would anchor the market’s expectations for the years that followed. The $24M Spyglass sale did not create the 2022–2025 market; it confirmed that the buyer pool for that market already existed.

By the fourth quarter of 2021, the average $/SF had reached $940 on 19 transactions. The community had gone from $452/SF to $940/SF in six years. More significantly, the $5M+ tier had expanded from 10 sales in 2015–2018 combined to 35 sales in 2021 alone.

Phase IV: The Value Era (2022–Present)

2022 is the most counterintuitive year in the dataset. Volume halved, 45 sales versus 89 in 2021. By conventional reading, a 49% drop in transaction count signals a market softening. What actually happened was the opposite. Average $/SF jumped from $775 to $1,133, a 46.3% increase, the largest single-year gain in the community’s recorded history. The buyers who transacted in 2022 were paying dramatically more per square foot on dramatically fewer homes. Scarcity was being priced in.

The mechanism is straightforward: the buyers who arrived in 2022 were not discouraged by higher prices. They were arriving because of what the asset had become. A community that had traded at $452/SF in 2015 and $631/SF in 2020 was now a community where the right home commanded $1,000–$1,600/SF. The buyer pool had shifted from buyers of Jupiter waterfront to buyers of South Florida trophy waterfront: a meaningfully smaller, meaningfully wealthier pool that does not negotiate on quality.

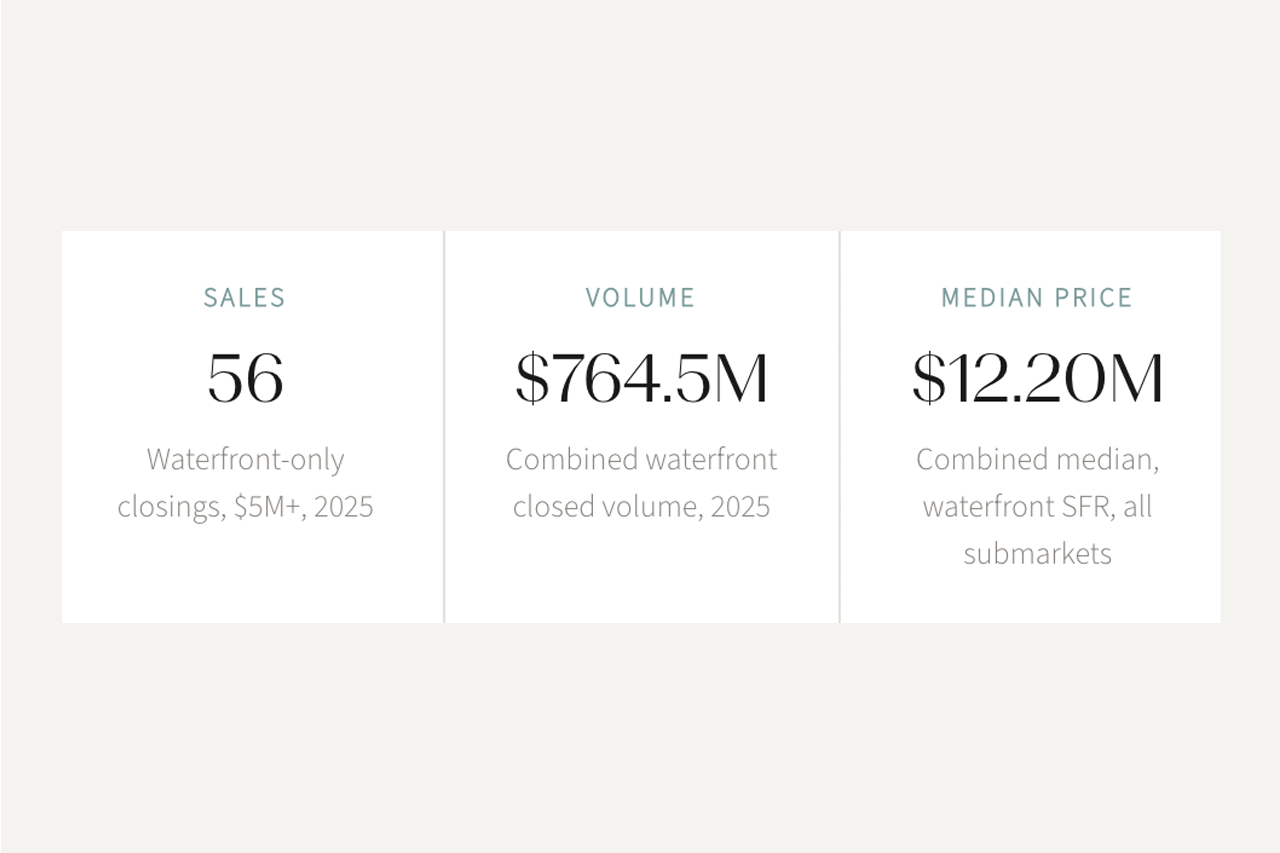

2023 through 2025 continued the appreciation at a calmer pace: +18.0%, +14.6%, and a near-flat +0.2% as 2025 settled. The community appears to be in a period of consolidation at the $1,500+/SF level. The median closed price crossed $5 million for the first time in 2023, crossed $5.5 million in 2024, and reached $6 million in 2025. The $10M+ tier, nonexistent before 2019, closed 7 transactions in 2023, 11 in 2024, and 12 in 2025.

The mechanism that will sustain the floor going forward is new construction. The market has accepted $15 million as the clearing price for a newly built canal-access home on a half-acre lot in Admirals Cove. That is not a ceiling; it is a reference point. When buyers can underwrite new construction at $15 million, resale inventory at $8–$12 million does not look expensive. New construction sets the upper bound of what the community is worth, and that upper bound continues to move. As long as land-constrained, permit-intensive waterfront communities like this one remain the only way to deliver that product in Jupiter, the resale market prices accordingly.

* 2022: market inflection year. Largest single-year $/SF gain on record (+46.3%) on the lowest volume since 2015 (45 sales). $10M+ counts reflect unique closed transactions (deduplicated MLS records). Source: BeachesMLS, extracted February 2026.

The Complete Repricing: How the Tier Distribution Transformed

The most vivid way to see what happened to Admirals Cove is not the $/SF chart but the tier shift. In 2015–2017, over a third of all sales closed below $1 million; these were typically smaller canal-access properties or units at the community’s entry tier, and their presence kept the median anchored in the low $1M range. By 2023–2025, that tier has completely disappeared. Not compressed: eliminated. Zero closings below $1 million in the last three years of data.

The movement at both ends of the distribution tells the story most clearly. The bottom has vanished and the top has exploded. In 2015–2017, zero percent of Admirals Cove closings came in above $10 million. In 2023–2025, 25 percent did, one of every four transactions. A community that was predominantly a $1–3M market has become predominantly a $5–10M market with a substantial and growing $10M+ segment. The center of gravity has shifted by approximately $4 million over a decade.

The most concrete way to see the repricing is through equivalent dollar amounts at different points in time. In 2015, $2.5–3.5 million bought genuinely substantial waterfront homes on main canals: 375 Eagle Drive closed at $345/SF, 476 Mariner at $415/SF; large lots, full waterfront access, community-comparable product. In 2025, the same $2.5–3.5 million buys either a non-waterfront home, a smaller canal-access villa, or a townhome-style residence on Captains Way at $963–$1,291/SF. The dollar amount hasn’t changed. The community has.

The Defining Transaction: 209 Commodore Drive

In November 2024, 209 Commodore Drive closed at $34 million, the highest price in Admirals Cove history and, at the time of closing, one of the highest residential sales in Jupiter’s recorded history. The transaction was not an outlier in the way that Bears Club’s $48 million close was; it was the logical culmination of a community that had been systematically repricing its flagship waterfront inventory for a decade.

A waterfront compound on Admirals Cove’s most prestigious corridor. Offered at $39.9M; now listed again at the same ask following a brief period off-market. The November 2024 close at $34M represents the clearest single data point for where the community’s flagship product prices today.

The $34 million close validated a sequence: 176 Spyglass at $24M in 2021 set the ceiling; the 2022–2023 repricing established $1,500–$2,500/SF as the waterfront premium range; and 209 Commodore at $1,398/SF on 24,320 SF confirmed that large-format waterfront estates in this community now transact in the low-to-mid eight figures without requiring anomalous buyer conditions to close.

Bottom Line

The repricing is durable because its mechanism has changed. Admirals Cove is no longer appreciating through volume; it is holding value through the composition of its buyer pool. The $10M+ tier is not an anomaly at the top of the market; it is now the market’s primary capital formation engine, and that structural shift does not reverse when interest rates move or seasonal demand softens. For buyers, the practical consequence is that the community no longer has a tier that absorbs demand at a discount: every entry point now prices the asset for what it has become. A flat year after three consecutive years of double-digit gains is the normal behavior of a market establishing a new floor, not a market signaling a correction.

For sellers at $5M+: The 2025 data confirms consolidation at the repriced level, not deterioration. If your hold thesis required further acceleration, the evidence does not support urgency. If your hold thesis is capital preservation at a durable floor, the year-over-year data validates it. Preparation and timing still matter; reach out to discuss where your specific asset sits within the tier.

For buyers considering entry at $2M–$5M: This tier no longer buys what it bought in 2017. The same dollars now access a smaller, non-waterfront, or townhome-format product. That is not a reason to avoid the community; it is the information needed to set accurate expectations, underwrite correctly, and identify where genuine value remains within the tier.

The contrarian read on 2025’s flat appreciation: A near-zero $/SF gain reads as stagnation. It is more accurately described as a community with over $2.6 billion in transactional precedent absorbing a decade of repricing at a level where structural demand, not momentum, is now the price floor. The next phase will be written by how the $10M+ tier performs, not by whether the entry tier recovers.

Data: BeachesMLS, extracted February 2026. All closed residential sales above $500,000 at Admirals Cove subdivisions, Jupiter, FL, 2015–2025. n=599 transactions.

$/SF calculation: All $/SF figures use the MLS Sold Price/SqFt field, which reflects the ratio of Sold Price to MLS-reported living area (SqFt - Living). Transaction-level averages across each calendar year or period are used throughout; these are not averages of annual averages. The 2015 and 2025 endpoint figures ($452 and $1,535/SF) are both transaction-level annual means. The decade appreciation of +240% is calculated as (1535−452)/452 using single-year endpoints.

Appreciation figure vs. comparison series: A companion article reports Admirals Cove appreciation as +208%, using a 2015–2016 pooled baseline ($473/SF, 70 sales) against a 2023–2025 pooled peak ($1,454/SF, 161 sales). That method pools two years at each end to reduce single-year variance and is appropriate when comparing two communities on equal footing. This article uses single-year endpoints (2015 vs. 2025) and produces the +240% figure. Both calculations are correct; they answer different questions. Readers of both articles should note the methodological difference.

$10M+ counts: Duplicate MLS records for the same transaction have been identified by matching address, price, and sale date, and removed. All $10M+ counts reflect unique closed transactions only.

Phase definitions: Phase I (2015–2018), Phase II (2019–2020), Phase III (2021), Phase IV (2022–2025) defined by the author to capture distinct mechanisms of appreciation visible in the data. Phase boundaries are analytical, not industry-standard designations.

Record sale (209 Commodore): 24,320 SF living area, 31,369 SF total area, 48,983 SF lot, 300+ ft waterfrontage, 9 bedrooms, 13 full baths, 1 half bath, 6-car garage, 2 docks. Source: MLS Tax Rolls.

Price tier distribution: Calculated as the percentage of closed sales in each price band within each time period. Era boundaries: 2015–2017 (n=106 sales), 2018–2020 (n=193 sales), 2021–2022 (n=134 sales), 2023–2025 (n=161 sales). All percentages rounded to nearest whole percent.

Median prices: True statistical medians of all closed transactions in each year, verified against source data.

Directional characterizations regarding buyer pool composition and cash share reflect practitioner observation across BeachesMLS closed data. These are directional characterizations, not formal statistical extracts. Figures vary by submarket and period and should not be applied to individual property underwriting without direct MLS comp analysis.

BeachesMLS / Beaches MLS Association of Realtors. Closed residential sales data, Jupiter FL, 2015–2025, extracted February 2026.

MLS Tax Rolls. 209 Commodore Drive property specifications, Jupiter FL.