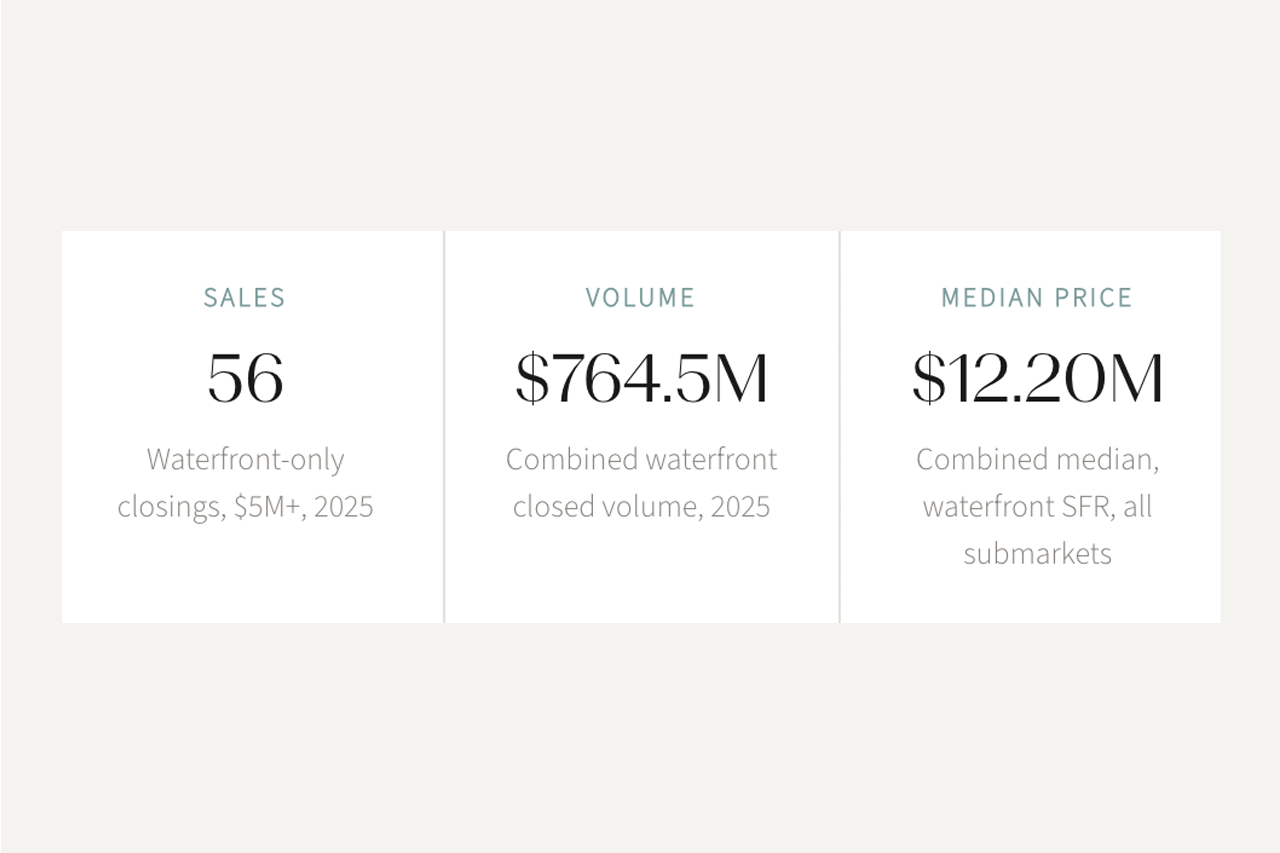

Start with the Water, Not the Kitchen

Most relocation stories begin with lifestyle: a boat, ten minutes from the inlet, waking up to water. Those ambitions are shaped, sometimes sharply, by physics and regulation. On Jupiter's Loxahatchee River and the Intracoastal, your usable world is defined by four things that no renovation budget can change after the fact.

A family arriving from New York with a 38-foot center-console may fall in love with a beautifully staged upriver home, only to discover that a low fixed bridge or shallow bend quietly disqualifies their boat. They can renovate the kitchen. They cannot change concrete and bottom contour. The correct renovation sequence for that family is: commission a recent depth survey, engineer lifts and pilings to suit their vessel and likely future upgrades, ensure shore power and water service at the dock, and only then begin debating cabinetry.

That process builds a house around the way they actually plan to use the water, and it stabilizes resale value because the next buyer is likely to share the same functional needs.

The Unseen Structure That Decides Your Insurance

The second layer of value is less visible than stone or millwork but more important for your balance sheet: the building envelope. Since FEMA's updated maps took effect in December 2024 and insurers tightened their criteria, three questions now dominate underwriting for coastal homes. The answers to all three belong in the renovation brief before a single finish is selected.

A relocation buyer who spends $400,000 on imported finishes but leaves an aging roof and unprotected sliders untouched often discovers, too late, that the renovation did nothing to widen their pool of willing carriers. In some cases, it makes the property harder to insure because the uplifted interior finish drives replacement-cost assumptions higher without improving the underwriting profile.

A Palm Beach couple bought a dated but well-sited Jupiter riverfront house three years ago. Their first move was a new code-compliant roof, impact systems on every exterior opening, and mechanical equipment re-sited above BFE. Only then did they slowly modernize interiors in phases. When they quietly explored a sale this year, their property drew interest from multiple out-of-state buyers, not because the kitchen was on trend, but because the documents told a clear story: insurable, elevated, and prepared for the current regulatory regime. In today's market, that is a premium asset.

Planning Renovation Capital with a Realistic ROI

Ultra-prime coastal property is not a spreadsheet exercise; nobody should expect a perfect one-to-one recovery on every dollar of renovation spend. But there is a hierarchy of return that tends to repeat in Jupiter, Jupiter Island, and the North End of Palm Beach. We advise clients to think in three distinct buckets, each with a different ROI profile and a different relationship to resale.

Investments that make the property insurable, dockable, and code-current. These are non-negotiable for maintaining the asset's place in the buyer pool. They tend to compress drawdowns and support values through regulatory cycles.

Investments that broaden the buyer pool by improving how the property reads during a showing. A buyer who can understand the view, the plan, and the potential within five minutes is a buyer who moves faster and with better terms.

Materials and features that are primarily for you. Exotic stone, hyper-specific fixtures, one-off built-ins. They make life pleasant but tend to be idiosyncratic at resale. Spend here, but recognize these are closer to consumption than infrastructure.

You can spend meaningfully in all three buckets. Knowing which is which sets expectations around ROI and prevents the most common renovation mistake, which is treating Bucket 3 as if it were Bucket 1.

Right capacity, beam allowance, and configuration for today's and tomorrow's boats. Not just a lift; the correct lift, calibrated to the vessel set and to likely future upgrades.

Roof, openings, and mechanical relocation to bring the property into alignment with current code expectations and updated FEMA maps. The foundational document for every insurance conversation.

Legal mangrove windowing, thoughtful rail and sill profiles, interior changes that connect main living spaces to the water in one clear glance. Broadens buyer pool and compresses time on market.

Removing visual and structural clutter so a buyer understands circulation, privacy, and potential within the first five minutes of a showing. Often achievable without structural changes.

Marble, stone, appliances, custom built-ins. Make life pleasant. Tend to be idiosyncratic at resale. Spend here after Buckets 1 and 2 are fully funded, not instead of them.

Three Scenarios We See Again and Again

The sequencing principles above play out differently depending on the buyer profile. Three patterns repeat with enough consistency that they are worth framing explicitly, both to recognize your own situation and to understand what the winning path typically looks like for each.

Relocation Realities Before You Sign

For those still at the planning stage, looking at Jupiter from New York, Chicago, London, or São Paulo, there are five realities worth acknowledging before a contract is written. None of them are dealbreakers. All of them are better understood in advance than discovered mid-diligence.

Bottom Line

The quiet logic behind Jupiter waterfront renovation runs counter to the instinct of most buyers arriving from other markets. Infrastructure capex (dockage, envelope, elevation, systems) determines whether a property remains insurable, dockable, and marketable as regulations evolve. Liquidity capex (view corridors, plan clarity, interior-to-water connection) broadens the buyer pool and compresses time on market. Both categories consistently outperform lifestyle capex at resale.

For relocation buyers from out of state: Start from the waterline. Commission the depth survey, engineer the dock and lifts for your five-year vessel plan, and replace the roof and openings before touching a single interior finish. The insurance document is the asset that unlocks everything else. Phase interiors around seasons; the kitchen can wait, but the carrier conversation cannot.

For Florida families upgrading to waterfront: Buy the location and the structure, phase the cosmetics. Model insurance before you commit. Budget first for the non-negotiable upgrades (roof, impact, mechanical elevation), then allocate remaining funds to view corridors and plan clarity. The ROI here is less about future appreciation and more about avoiding negative surprises as carrier appetites evolve.

For sellers preparing a waterfront listing: The renovation that matters most for your exit is the one the next buyer's insurance broker will evaluate, not the one their interior designer will admire. Resolve the envelope, document the mitigation, and confirm route-to-ocean before photography. A property with a clean underwriting story and a confirmed dockage profile attracts a wider audience and holds pricing power that erodes with every unresolved diligence item on market.

This article draws on closed transaction data from the Palm Beach MLS (2020–2024), renovation cost ranges sourced from Palm Beach County-licensed contractors active in Jupiter and Jupiter Island, and insurance underwriting criteria as disclosed by admitted and surplus-lines carriers operating in coastal Florida as of Q4 2024. FEMA flood map references reflect the December 2024 update to Palm Beach County's Flood Insurance Rate Maps (FIRMs).

Renovation ROI characterizations (Infrastructure, Liquidity, Lifestyle) represent directional guidance based on observed resale outcomes in the Jupiter and Jupiter Island waterfront segments and are not a guarantee of future performance. Individual results will vary based on property condition, market timing, buyer profile, and scope of work. This article does not constitute legal, tax, engineering, insurance, or investment advice. Consult qualified professionals before making any renovation, acquisition, or disposition decision.

Equal Housing Opportunity.

Transaction data: Realtors Association of the Palm Beaches / Beaches MLS, closed sales 2020–2024, filtered to Jupiter and Jupiter Island waterfront single-family residential.

Flood mapping: Federal Emergency Management Agency (FEMA), Flood Insurance Rate Map revisions effective December 2024, Palm Beach County, Florida.

Insurance underwriting criteria: Carrier disclosure documentation and broker guidance from admitted and surplus-lines markets operating in coastal Palm Beach County, Q3–Q4 2024.

Renovation cost ranges: Field estimates from Palm Beach County-licensed general contractors and marine contractors active in Jupiter, Tequesta, and Jupiter Island, 2023–2024.

Dockage and permitting frameworks: Florida Department of Environmental Protection (FDEP) and U.S. Army Corps of Engineers Section 404/10 permit guidelines; Town of Jupiter and Palm Beach County marine construction regulations.

Mangrove trimming rules: Florida Statute 403.9326 and associated DEP rule 62-340, governing mangrove alteration by property owners and licensed professionals.