The dataset covers 3,446 closed single-family detached sales at $1M and above across both markets from 2020 through 2025, split between the Jupiter corridor (zip codes 33458, 33469, 33477, 33478) and Palm Beach Island (33480). For each transaction, we track sold price, living square footage, price per square foot, and days on market. The two markets differ fundamentally in price distribution, product type, and buyer profile. Jupiter's volume is concentrated between $1M and $2M; Palm Beach Island's median exceeds $13M. A raw comparison of medians would obscure more than it reveals, so the analysis segments by price tier to isolate the range where the buyer pools actually overlap.

The Shift North

For decades, Florida's luxury conversation began and ended in Miami or on the island of Palm Beach. In the last five years, a measurable share of the capital that once concentrated in those corridors has moved north toward Jupiter. The migration draws disproportionately from entrepreneurs, family offices, and financial professionals who prioritize privacy, space, and daily livability over social infrastructure and institutional address recognition. The profile is specific, and it matters for understanding both the demand driver and the liquidity structure of the market.

Zoning restraint has preserved both the landscape and the character of the corridor. Environmental overlays along the Indian River Lagoon, coastal construction setbacks, and the absence of any high-rise zoning corridor produce a supply constraint that is legislative and permanent. It does not fluctuate with interest rates or development sentiment. It is embedded in the regulatory framework and reinforced by federal conservation designations that predate the current demand wave.

Jonathan Dickinson State Park encompasses roughly 11,500 acres immediately north of Jupiter and cannot be converted to residential use. Combined with the Loxahatchee River's Wild and Scenic federal designation (which prohibits dredging, fill, and commercial development along its corridor), the conservation buffer around Jupiter is among the most protective in any Florida luxury submarket. These designations are not subject to reversal by local zoning action.

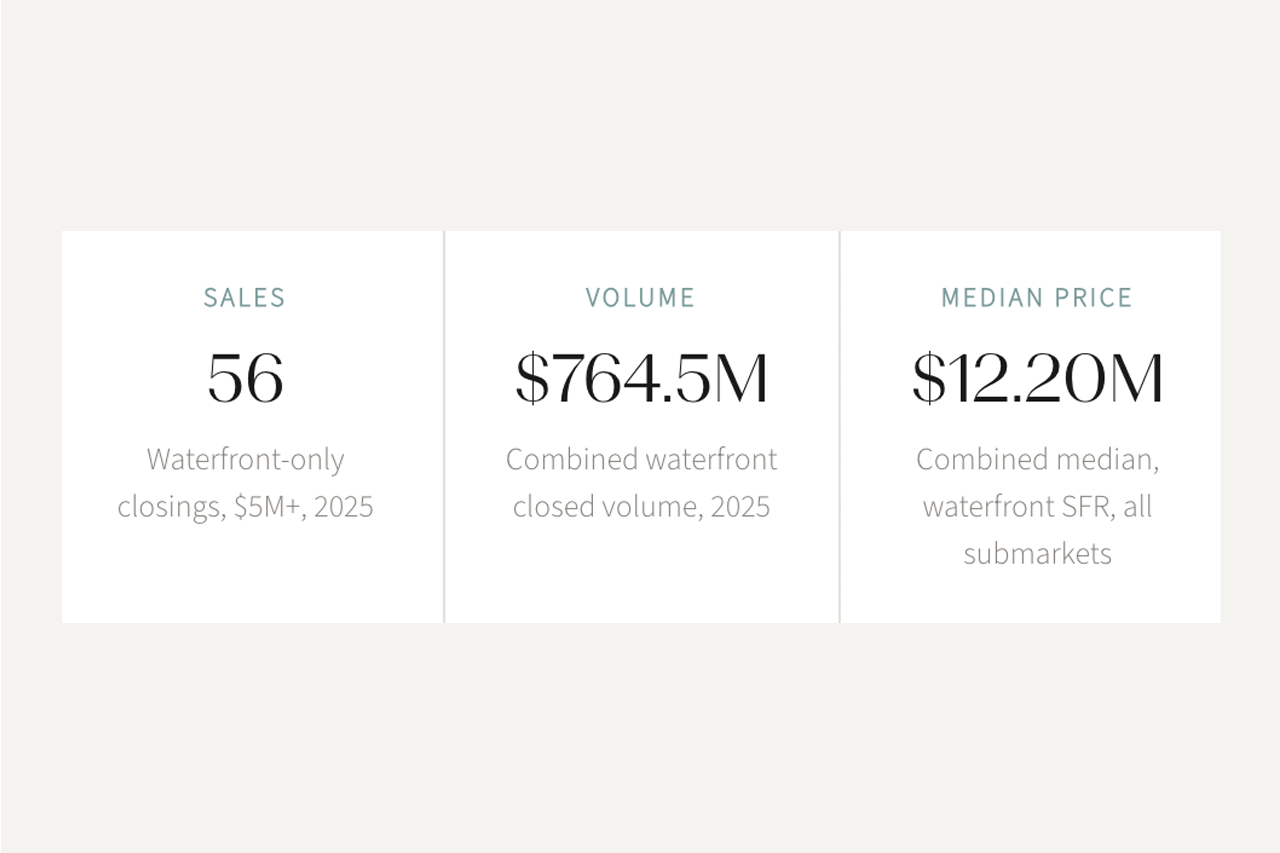

Two Markets, Not One Discount

The most common shorthand for comparing Jupiter and Palm Beach Island is a percentage discount. That framing is misleading. These are fundamentally different markets serving different buyer priorities, with different price distributions, different product types, and different liquidity profiles. Comparing raw medians produces a gap of 65 to 87 percent, but the number is meaningless because the underlying product is not comparable: 60 percent of Jupiter's volume transacts between $1M and $2M, while the island has zero closed sales below $3M.

The comparison only becomes useful when segmented to the price tier where the buyer pools actually overlap. At $5M and above, both markets produce meaningful transaction volume and the data reveals what each market delivers per dollar.

Source: BeachesMLS closed sales, SFD $5M+, Jupiter corridor.

Source: BeachesMLS closed sales, SFD $5M+, Palm Beach Island (33480).

The tables reveal a structural difference, not a simple discount. In 2025, a buyer deploying $8.3M in Jupiter acquired a median 5,986 square feet at $1,642 per square foot. The same capital on the island would fall below the $13.85M median and purchase a materially smaller home at $3,005 per square foot. Jupiter delivers more house. The island delivers a different kind of value: a globally recognized address, a deeper resale pool at the top of the market, and proximity to social infrastructure that Jupiter does not replicate. The data does not declare a winner. It defines what each market provides at comparable capital deployment.

A note on the comparison: Median figures reflect the mix of properties transacting in each market and year. In small-sample tiers, one or two outlier transactions can shift the median materially. The data should be read as directional market characterization, not as implied returns or guaranteed pricing for any individual property. Direct comp analysis is required for property-level underwriting.

A Geography of Balance

The Jupiter Inlet divides the Atlantic Ocean from the Indian River Lagoon, a meeting of open-ocean power and protected-water calm that defines the area's dual character. Between the golf enclaves to the west and the waterfront estates to the east lies a lifestyle that accommodates both motion and retreat, often within the same property. Out-of-state buyers consistently note that this corridor retains the texture of old Florida while delivering contemporary infrastructure and access.

Private golf communities and equestrian enclaves set within manicured landscapes. Club life, open acreage, and the pace of a morning round. Representative communities include Admirals Cove, Jonathan's Landing, The Bear's Club, and Ibis Golf and Country Club.

Waterfront estates and mangrove preserves where natural buffer meets deep-water access. Tide charts, private docks, and the horizon as a daily constant. Key positions include Jupiter Inlet Colony, Admiralty, North Fork, and direct ICW and oceanfront parcels.

The Financial Case

For financial migrants, Florida's tax structure provides the initial logic for relocation. Jupiter provides the reason to stay. The absence of state income tax, combined with homestead protections and portability provisions, creates a meaningful annual carrying cost advantage over comparable addresses in the Northeast, California, and Illinois. The financial case is well established. The question that matters more is what a buyer actually receives for each dollar deployed in Jupiter versus the alternatives within Florida.

The financial calculus extends beyond the spreadsheet. The combination of more space, fewer people, direct water access, and a daily pace that accommodates both work and outdoor life is harder to replicate than any tax structure. Whether the pricing differential between these two markets reflects incomplete recognition of what Jupiter has become, or a fair discount for the trade-offs described below, depends on the buyer's own weighting of those variables. The data provides the framework. The decision is personal.

Architecture and Craft

The current generation of new construction in Jupiter favors native materials, biophilic design, and an emphasis on light and site orientation over ornament. Architects including Max Strang and René Gonzalez have catalyzed a wave of context-sensitive modernism across South Florida: stone, glass, and timber rendered in coastal harmony with the landscape rather than imposed upon it. The design language spreading through Jupiter's most considered estates is international in its references yet unmistakably Floridian in its relationship to water and site.

The shift from ornament to material integrity carries valuation implications. A residence built with imported stone, custom millwork, and site-specific orientation holds value differently than a finish-driven home. Jupiter is not unique in this shift (the same trend runs through Naples, Sarasota, and parts of Miami), but the combination of material quality and environmental setting is more pronounced here than in higher-density corridors. The homes being completed now will serve as the comparable set against which future inventory is measured.

Architectural quality supports long-term value, but it is not a substitute for location fundamentals. The strongest properties in the Jupiter corridor combine site-specific construction with the supply constraints described above: frontage on protected water, conservation adjacency, and the absence of developable land between the property and the natural buffer. A well-built home on a replicable lot is a different asset than a well-built home on an irreplaceable parcel. Buyers should underwrite the parcel before the house.

What the Trade-Offs Cost

Any advisory analysis that presents only the case for a market without presenting the case against it is promotional, not analytical. Jupiter offers real advantages. It also carries specific trade-offs that a buyer should model before committing.

Trade-Offs and Risk Factors

None of these trade-offs invalidates the case for Jupiter. They define its boundaries. A buyer who understands the trade-offs and values the lifestyle, the supply constraint, and the daily experience of ownership is making an informed decision. A buyer who assumes convergence without modeling the alternative is making a different kind of decision.

Bottom Line

The intro asked whether Jupiter and Palm Beach Island serve the same buyer. They do not. The data confirms what practitioners observe on the ground: these are structurally different markets with different products, different buyer profiles, and different value propositions. At $5M and above, where the pools overlap, Jupiter delivers materially more living space per dollar on larger parcels with a permanent supply constraint. The island delivers a deeper resale pool, a globally recognized address, and proximity to social infrastructure. The supply constraint in Jupiter is real, codified, and not reversing. The demand trajectory favors this corridor. Whether those fundamentals produce price convergence or simply defend a stable relationship between the two markets is the open question the data cannot yet answer. Both outcomes are plausible. Both should be modeled.

For buyers relocating from out of state at $5M to $15M: Model total carrying cost (purchase price plus insurance, property tax net of homestead, and maintenance) against your current jurisdiction. The tax savings are meaningful, but the insurance delta is larger than most Northeast buyers expect. Visit in summer, not season: the property you are buying is the one you will live in when the seasonal population is gone.

For buyers choosing between Jupiter and the island: The decision is not which market is better. It is which trade-off set matches your priorities. Jupiter offers more house, more land, direct water access, and a codified supply constraint at a lower price per square foot. The island offers a deeper resale pool, institutional recognition, and social infrastructure. If you are building a primary residence for a decade or more, Jupiter's fundamentals work in your favor. If you anticipate a shorter hold or value resale optionality, the island's deeper buyer pool is the more conservative position.

For sellers in the Jupiter corridor at $5M+: Price to like-kind comps and replacement-cost logic. In a market that produced 65 transactions at this tier last year, credibility generates competition and overpricing generates silence. Prepare the file before launch: wind-mit, 4-Point, elevation certificate, and preliminary insurance quotes remove the friction that erodes deals between contract and close.

General information only. This article is an editorial market perspective and does not constitute legal, tax, financial, or investment advice. Market characterizations, pricing references, and lifestyle descriptions reflect general observations and should not be relied upon as the basis for any financial or real estate decision.

Dataset. Transaction statistics reflect BeachesMLS closed sales, single-family detached, $1M and above, 2020 through 2025. Jupiter corridor: zip codes 33458, 33469, 33477, 33478 (2,852 transactions). Palm Beach Island: zip code 33480 (594 transactions). All metrics are derived from this filtered dataset.

Comparison methodology. Raw median comparisons across these two markets are misleading due to fundamental differences in price distribution and product type. Jupiter's volume is concentrated between $1M and $2M; Palm Beach Island's median exceeds $13M. The analysis segments to $5M+ to isolate the tier where buyer pools overlap. Even within that tier, product differences (home size, lot size, waterfront type) affect the comparison. The data should be read as directional market characterization, not as a like-for-like or apples-to-apples comparison. Direct comp analysis is required for property-level underwriting.

Supply constraint characterizations. References to permanent or structural supply constraints reflect the authors' assessment of current federal, state, and local regulatory designations. These designations are durable but not immutable. Regulatory changes, while unlikely, remain possible.

Tax information. Florida tax advantages described reflect general state policy as of publication date. Tax treatment depends on individual circumstances. Confirm all tax-related decisions with qualified legal and tax professionals.

Primary data: BeachesMLS closed and active listing data, Palm Beach County Property Appraiser records, Florida Department of Revenue homestead and portability guidelines.

Regulatory: Town of Jupiter zoning code, Palm Beach County Coastal Construction Control Line regulations, National Wild and Scenic Rivers System (Loxahatchee River designation), Florida DEP conservation overlays, Jonathan Dickinson State Park management plan.

Insurance: Florida Office of Insurance Regulation consumer resources, practitioner quoting experience across Jupiter waterfront and inland properties.

Market context: Practitioner transaction data and client advisory experience across Jupiter, Tequesta, Jupiter Inlet Colony, Palm Beach Island, and surrounding luxury submarkets.