This guide covers the enclave's fundamentals: scale, permit trends, pricing context, waterfront tiers, and a buyer's framework for evaluating opportunity in one of Palm Beach County's most supply-constrained addresses.

The Enclave, By the Numbers

Jupiter Inlet Colony is one of the smallest incorporated municipalities in Palm Beach County and one of the most deliberately preserved. Its constraint is structural: a fixed peninsula with a single road in and out, a municipal police force, and a housing stock that grows only through replacement. These are not incidental features. They are the conditions that make the place work as a long-term value proposition.

The translation for buyers is simple: fixed land, fixed streets, and a housing stock that renews through replacement rather than expansion. That is the classic precondition for compounding value over time, and it is why the Colony's price trajectory has been consistently upward across cycles that have been less kind to comparable markets.

Two Decades: From Beach Community to Ultra-Luxury Enclave

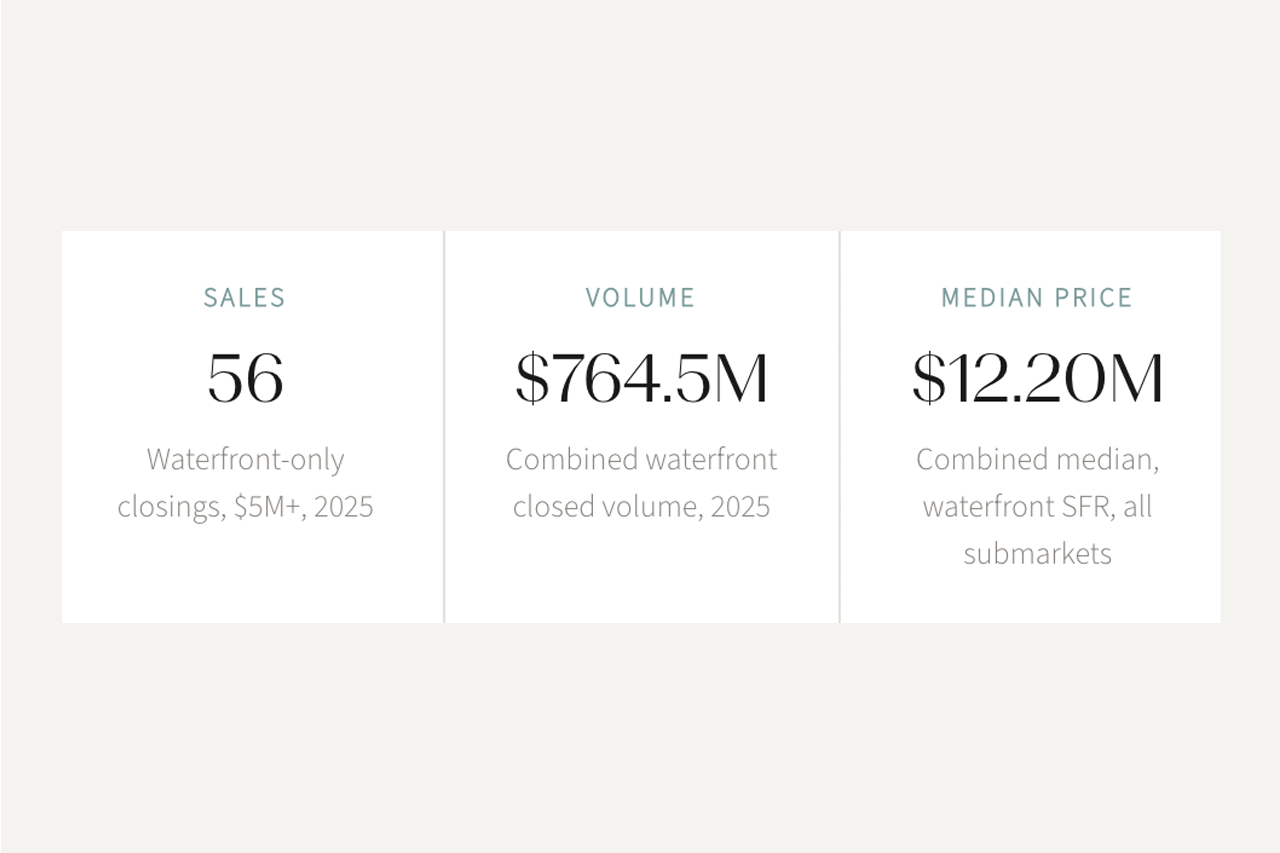

BeachesMLS closed transaction data from 2005 to present tells the full story. Jupiter Inlet Colony has undergone a structural transformation, from a sub-$1 million median beach community through the 2008 crisis, through a steady growth phase, and into the post-2020 era where the median has cleared $5 million and every transaction closes in cash. The data covers 252 closed single-family sales totaling $672 million across 21 years.

Source: BeachesMLS closed SFR transactions, Jupiter Inlet Colony, 2005 to present.

The inflection is visible across all three charts: a long plateau from 2005 through 2019 where the median oscillated between $625,000 and $1.6 million, followed by a structural repricing that tripled the median in three years. The third chart tells the institutional story: volume surged to 23 sales in 2020 as cash buyers arrived, then compressed to 7 in 2024 as the market repriced and inventory tightened. Meanwhile, cash share climbed from the 40 to 70 percent range to 100 percent. This is not a speculative cycle. It is a buyer-profile migration: leveraged local buyers replaced by unleveraged principals who relocated permanently and paid cash.

From the 2011 trough to the 2024 peak, the Colony's median sold price increased roughly eightfold: $625,000 to $5.275 million, a compound annual growth rate of approximately 17.8%. Per-square-foot pricing followed a similar trajectory, from $306 to $2,223. Two forces drove this simultaneously: the rebuild cycle (1970s ranches replaced by elevated, impact-glazed modern coastal construction that reset the comp set) and a structural migration of cash buyers from the Northeast and Midwest who discovered the Colony's combination of ocean access, Intracoastal dockage, and controlled entry. The appreciation is real, but it is not uniformly distributed: waterfront and new-construction parcels captured the majority of the upside, while unrenovated inland homes appreciated more modestly.

Waterfront Price Histories: Six Properties, Two Outcomes

The aggregate data tells the macro story. Individual properties tell the micro story, and it is often more compelling. Below are six waterfront addresses with documented repeat sales in the BeachesMLS record. Five illustrate the rebuild premium: properties that were torn down and rebuilt to modern specification, with returns ranging from 2.9x to 7.9x. The sixth illustrates the renovation ceiling: a high-quality renovation that appreciated well but topped out at a materially lower per-square-foot price than new construction on comparable frontage.

The rebuild premium is structural, not cosmetic. Every property that crossed $10 million involved either a full tear-down and rebuild or was already high-specification modern construction. New impact systems, elevated pads, and modern mechanical specifications are what buyers at this level require. 22 Ocean Drive illustrates the ceiling: renovated to a high standard but not rebuilt from the ground up, it peaked at $2,359 per square foot while new construction on the same streets cleared $2,726 to $3,690. The difference is not marginal. At 6,359 square feet, the gap between renovation pricing and new-construction pricing represents $2.3 million to $8.5 million in unrealized value. For sellers evaluating whether to renovate or rebuild before listing, the data is unambiguous.

New Construction Trends: Rebuilding, Not Expanding

In a built-out peninsula, building permits tell a specific story. The numbers are not about density; they are about the quality of replacement. When an owner tears down a 1970s ranch and builds an elevated, impact-glazed modern coastal residence, the door count stays the same but the comp set moves up. That is what the permit trend at Jupiter Inlet Colony represents.

Source: Palm Beach County annual and quarterly permit reports for Jupiter Inlet Colony. 2025 figures represent Q1 only.

A renovation-ready or tear-down property in Jupiter Inlet Colony is not a discount opportunity in the conventional sense; it is an entry point into a neighborhood where every new build raises the floor. The question is not whether to invest in the envelope; it is when and at what specification level. Buyers who wait for a finished product pay for the rebuild cycle they missed.

The cadence, rising from 3 to 9 to 11, signals owners reinvesting in better architecture, higher elevation pads, and superior envelope performance while total unit count stays capped. Each high-spec rebuild pulls the waterfront and near-waterfront comp set higher, resetting buyer expectations for the whole neighborhood without adding a single new address.

Pricing Context

The historical data establishes the trajectory. What it does not show is the gap between the broader housing stock and the waterfront tier, which is where the real pricing story lives. Unrenovated inland homes still trade in the low single-digit millions; waterfront and new construction routinely clear $5 million and above. Each high-specification rebuild resets the comp set for the entire neighborhood, and buyers pricing against three-year-old comps are working from an outdated floor.

The Waterfront Premium: Where Upward Pressure Is Most Visible

Water in Jupiter Inlet Colony works like a ratchet. Each cycle of high-specification replacement pulls the waterfront comp set higher and resets expectations for the neighborhood as a whole. When frontage is genuinely finite and new product is genuinely exceptional, the top of market re-prices quickly and durably. That dynamic has been running for five consecutive years, and the per-square-foot trajectory from $785 in 2020 to $2,223 in 2024 is the clearest measure of it.

Elemental drama: dune adjacency, direct Atlantic exposure, and short sand paths to the water's edge. Sunrise orientation with the full sensory range of the ocean at close range. The building envelope earns its specification here.

Premium driver: irreplaceable exposure and the emotional primacy of direct ocean frontage. Supply is finite by geography, not just zoning.

Active water with boat traffic, inlet energy, and proximity to open ocean. The visual scene changes hourly with tides and vessel movement. Proximity to the inlet mouth is both an amenity and an access point for boating families.

Premium driver: boating utility combined with the visual dynamism of active water. Verify current, setbacks, and dock feasibility by parcel before pricing the water premium.

Sheltered water, dockage potential, and the prolonged warmth of west-facing afternoon light. Calmer than the oceanfront, more usable for everyday boating, and better suited for dock configurations that require a settled approach.

Premium driver: dockage utility and the practical value of protected water. Not every parcel is dock-ready; setbacks, current, and orientation must be matched to vessel size and use before the water premium is quantified.

Match the Water to the Use Case Before the View

Inventory, Liquidity, and Timing

Because the Colony is so small, active listings at any given moment typically sit in the single digits to low teens. That thin inventory produces episodic pricing: long stretches of quiet activity punctuated by a high-water-mark sale that resets the comp curve for every subsequent transaction.

In a market this small, waiting for conditions to improve is a losing strategy. The right frontage, light orientation, and replacement quality do not appear on a schedule; they appear when they appear. Buyers who are not prepared to move quickly when the right property surfaces do not miss a good deal. They miss the deal. Preparation means proof of funds current, financing pre-underwritten, and inspection specialists identified before the listing appears.

Architecture ranges from renovated mid-century ranch to modern coastal new-builds with elevated pads, impact systems, and native landscape. Scale stays humane; replacements signal higher craftsmanship, not greater density. The everyday luxury is proximity: sand at dawn, Intracoastal glow at dinner, and security that operates discreetly and locally.

A Buyer's Framework

Jupiter Inlet Colony rewards buyers who approach it with a clear set of priorities established before the first tour. In a market with this few active listings, the decision framework needs to be complete before the right property surfaces, not developed in response to it.

East orientation delivers the sunrise ritual that defines oceanfront living here. West orientation delivers prolonged afternoon warmth over calm Intracoastal water. Know which cadence you are buying before you evaluate a floor plan.

Landscape depth, setback configuration, and courtyard planning matter as much as bedroom count at this price tier. The Colony's low density creates natural privacy, but parcel orientation and neighbor proximity vary. Evaluate the site plan as carefully as the floor plan.

Oceanfront for sand and elemental drama. Intracoastal for dockage and the reliability of sheltered water. Inlet frontage for energy, views, and proximity to open water. Each carries a different specification requirement and a different buyer profile.

One entry point and a dedicated municipal police presence are not incidental features; they are the operational conditions that make the Colony feel like a private compound rather than a public neighborhood. That calm is worth pricing in.

Elevation pad, impact glazing, roof deck attachment, and secondary water barrier are not luxury upgrades in this location; they are the baseline for insurability, comfort, and long-term value retention. Prioritize envelope quality over finish level.

In small, preserved enclaves with fixed supply and a compounding rebuild cycle, the buyers who hold longest typically fare best. Entry price matters, but the quality of what you buy and the integrity of the envelope you buy it in matters more over a ten-year horizon.

Bottom Line

Jupiter Inlet Colony is not a compromise between ocean living and Intracoastal living; it is the rare address where both are available within a few hundred feet of each other, within a community scaled to human life rather than development economics. Fixed supply, a single entry point, and a compounding rebuild cycle are not incidental characteristics. They are the investment thesis expressed as a neighborhood.

The practical implication: timing matters less than preparation. Active inventory sits in the single digits. Buyers who arrive prepared, with proof of funds current, financing pre-underwritten, and waterfront due diligence specialists identified, are the ones who close when the right property surfaces.

For buyers evaluating oceanfront parcels: The emotional premium is real, but so is the specification requirement. Storm exposure, elevation, and glazing performance define both insurability and long-term value. Lead with the envelope assessment, not the view. The view is permanent; the question is whether the structure earns the right to sit in front of it.

For buyers evaluating Intracoastal and inlet-side parcels: Dock feasibility, current speed, setbacks, and water depth at mean low water vary significantly by parcel. A survey and depth sounding belong in the file before the offer, not after. Protected water and functional dockage are the premium drivers here, and the practical value of everyday boating utility compounds over a long hold period.

For all buyers in this enclave: In small, preserved enclaves, quality compounds while supply stays finite. The best time to be prepared was before the listing appeared. Define your water type, your privacy brief, and your envelope standard now. When the right parcel surfaces, the buyers who move with clean terms and a complete file are the ones who close. Everyone else watches.

Historical market data reflects BeachesMLS closed single-family residential transactions for Jupiter Inlet Colony, 2005 to present. The dataset covers 252 closed sales totaling approximately $672 million. All figures are property-level closed sale data. Era summaries (Pre-Crisis, Downturn/Recovery, Growth, Transformation) use median and mean calculations across the stated year ranges. Compound annual growth rate calculations reflect point-to-point measurement from 2011 trough to 2024 peak and should not be extrapolated as forward projections.

Permit data reflects single-family dwelling permits approved by the Town of Jupiter Inlet Colony as reported in Palm Beach County annual and quarterly permit summaries. 2025 figures represent Q1 only and are not annualized.

Population and household figures are drawn from ACS estimates via DataUSA and Census Reporter. These are survey-based estimates and may differ from municipal records.

Pricing context references BeachesMLS closed transaction data and practitioner observation. In a market with single-digit to low-teen active listings, individual transactions move index values materially. Treat directional ranges, not specific figures, as the relevant signal for underwriting purposes.

The $30.18 million town-record sale referenced reflects a closed transaction at 103 Lighthouse Drive in 2024, per BeachesMLS records.

Historical market data: BeachesMLS closed single-family residential transactions, Jupiter Inlet Colony (Area 5030), 2005 to present. 252 closed sales, property-level data.

Permit activity (single-family units): Palm Beach County annual and quarterly permit reports for Jupiter Inlet Colony. 3 (2022 Annual Report), 9 (2023 Annual Report), 11 (2024 Annual Report); 2025 Q1: 3 (2025 Q1 Permit Activity Report). discover.pbcgov.org/pzb/planning

Scale and households: ACS/DataUSA, population ~486, ~204 households. datausa.io/profile/geo/jupiter-inlet-colony-fl

Town footprint and density: Census Reporter, approximately 0.2 sq mi, population 486. censusreporter.org/profiles/16000US1236250-jupiter-inlet-colony-fl/

Municipal police and single-entry culture: Town of Jupiter Inlet Colony Police pages. jupiterinletcolony.gov/346/Police

Pricing context: BeachesMLS closed transaction data, Palm Beach County. Practitioner observation, Palm Beach Luxury at Compass.