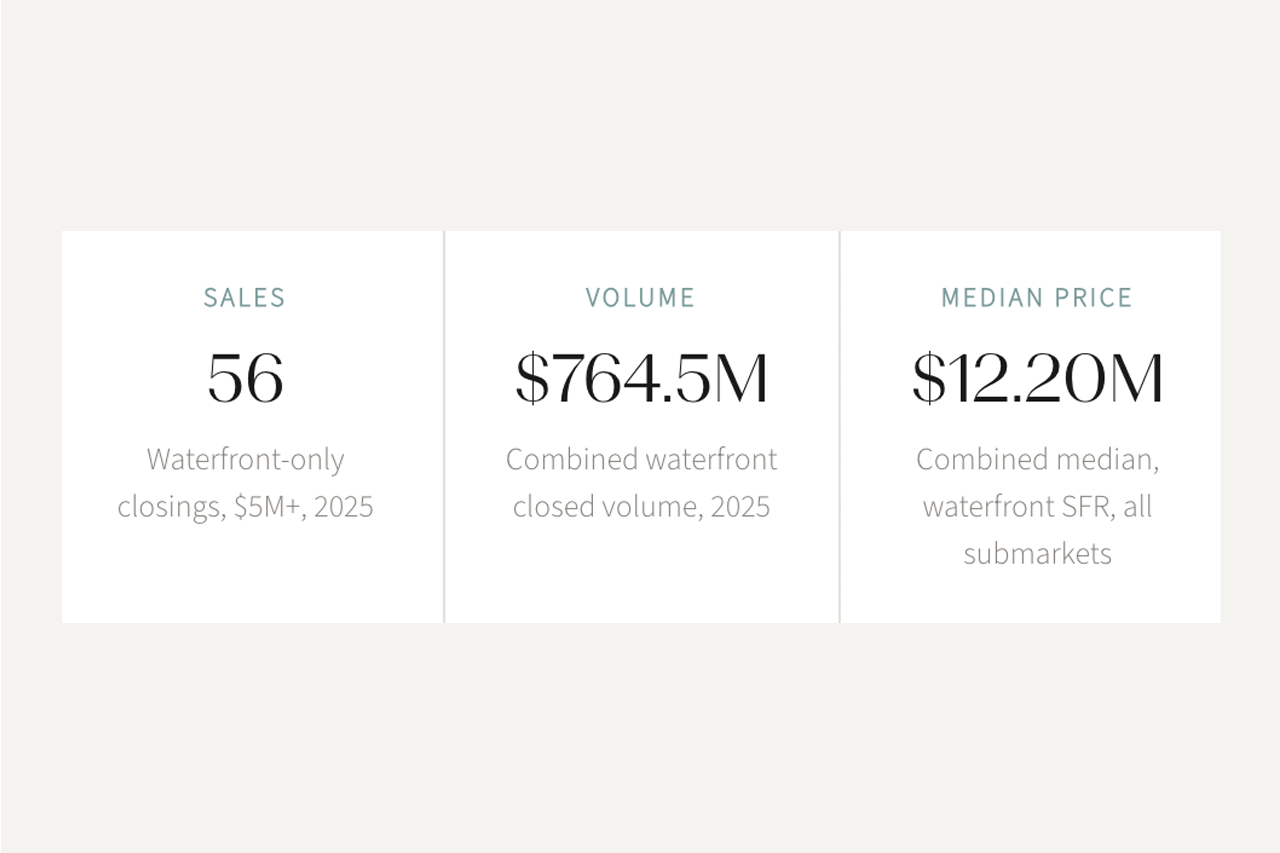

The dataset covers 1,008 closed sales from 2016 through 2025, filtered to Intracoastal, river, ocean, and ocean-access canal frontage, sourced from BeachesMLS. For each transaction, we track closing price, price per square foot, and days on market, then segment by year. Median prices over the period rose from $1.19M to $4.28M, a compound annual rate of 15.3%, while annual transaction volume never exceeded 142 closed sales in any single year. That combination, durable appreciation on thin volume, is the defining characteristic of this corridor and the starting point for the analysis that follows.

Market Mechanics: How Conservation Creates Structural Scarcity

The condition of Jupiter's waterfront market is not accidental. Federal Wild and Scenic River designation for the Loxahatchee, state and private conservation of the adjacent shoreline at Blowing Rocks, and local planning frameworks that have consistently resisted Palm Beach County's density norms have produced a market where the supply constraint is structural. It does not fluctuate with interest rates or development sentiment. It is embedded in the land itself.

MLS closed sales, single-family detached, Intracoastal / river / ocean / ocean-access canal. Zip codes 33458, 33469, 33477, 33478.

New inventory comes not from raw land but from resale of existing properties, each transaction anchored in comparable evidence rather than developer pro forma math. The parcels fronting the Intracoastal, the river, and the ocean are largely in place. The release valve does not exist here. A note on methodology: median price movement on a sample this thin reflects both underlying property-level appreciation and compositional shifts in the mix of properties transacting each year. If higher-value oceanfront closes disproportionately in one year and lower-value canal-front in another, the median moves independently of any single property's value trajectory. The figures above should be read as market-level indicators, not as implied returns on any individual parcel.

Source: MLS closed sales, Jupiter SFD Intracoastal / river / ocean / ocean-access canal waterfront, 2016 to 2025.

The Loxahatchee is the only federally designated Wild and Scenic River in Florida. Blowing Rocks Preserve spans roughly 700 acres of Jupiter Island from the Atlantic beach to the Intracoastal, a parcel that will not convert to residential use. Jonathan Dickinson State Park adds approximately 11,500 acres of permanently protected land adjacent to the river corridor. Low-density planning in Jupiter and Tequesta caps what can be built on the parcels that remain.

For buyers, the scarcity they are purchasing is real and unlikely to erode. For sellers, corrections tend to be shorter-lived and followed by faster recoveries than in supply-rich environments, a function of thin transaction volume rather than immunity to market forces. That asymmetry is what distinguishes Jupiter waterfront from corridors where supply can and does grow.

Jupiter, Tequesta and Jupiter Inlet Colony: Three Distinct Water Experiences

Describing Jupiter waterfront as a single market obscures meaningful differences between the three principal nodes. Each has a distinct relationship with the water in terms of exposure, inventory depth, access profile, and the daily experience of ownership.

Sheltered Intracoastal and river basins reward daily use; west-facing light defines dusk on the water. Oceanfront carries sunrise ritual and elemental exposure. The inlet stitches the two environments together, but conditions evolve with tide and sand transport. Vessel sizing and lift choices should be conservative. The broadest inventory and widest range of format among the three submarkets.

Leafy streets and mangrove edges that translate to privacy and calm. Inventory is micro: there are simply not many properties, and new supply does not come from undeveloped land. Replacement trends toward better envelope performance, not more units. Architectural quality rises while scarcity endures. The buyer pool skews toward those who recognize that low transaction velocity is a feature.

At the southern tip of Jupiter Island, inlet views and ocean proximity define the mood. Private dock scenarios exist where geometry allows; marina-first strategies can be optimal for larger draft profiles. A small, incorporated community where transaction cadence is deliberately unhurried. Buyers arriving without a relationship to the community often benefit from guidance before making first contact.

A buyer whose priority is dock-and-go access for a 40-foot vessel with a five-foot draft will find very different answers in each submarket. Jupiter's basins and draw-bridge schedules may be optimal; Jupiter Inlet Colony's marina access may be more constrained. Running the access audit before committing to a geography, rather than after, is one of the most consequential early decisions in the search process.

Access, Bridges and the Water Reality

Water access is not simply an amenity in this market. The frequency and ease with which a property supports actual time on the water is a measurable component of value, both at purchase and at resale. Understanding the specific access profile requires going beyond the listing and onto the water.

Waterfront Access: What to Verify Before You Contract

The single most underused step in a Jupiter waterfront purchase is a pre-offer water tour of the route from the subject property to open ocean. Run it at displacement speed and at planing speed. Note bridge wait times and clearances. Check inlet conditions on a representative day. The information revealed in ninety minutes on the water is not available in any listing, disclosure, or survey.

Buyer and Seller Playbook

Jupiter waterfront transactions do not behave like standard residential transactions. The market's combination of thin inventory, experienced participants, and a well-established broker community means that process matters as much as price.

The underlying logic on both sides is the same: in a market defined by thin inventory, process efficiency is a competitive advantage. Buyers who move quickly and cleanly win properties they otherwise lose. Sellers who launch with credibility and a prepared file compress time on market and protect net proceeds.

Risk and Insurance Realities

Florida waterfront insurance is not a commodity. The premium for a Jupiter waterfront property is derived from the specific combination of construction type, elevation certificate, roof age and attachment method, opening protection, proximity to the inlet or ICW, and current carrier appetite in that census tract. Two adjacent properties with similar aesthetics can produce meaningfully different insurance outcomes. Discovering this at closing is late.

For buyers, insurance feasibility is a search filter, not a closing condition. A property that cannot be bound at a premium consistent with the buyer's total carrying cost expectation is not a viable candidate. For sellers, a property that has been pre-quoted (with wind-mit report, 4-Point, and elevation certificate available from day one) removes the most common source of late-stage deal erosion in Jupiter waterfront transactions.

Tax and Ownership Notes

Florida's tax framework for residential real estate offers meaningful benefits to eligible owners. None of the following constitutes legal or tax advice; coordinate structure and filings with your attorney and CPA before committing.

One nuance for waterfront buyers: ownership structure (LLC, trust, or individual) can affect both homestead eligibility and the mechanics of documentary stamp. For buyers planning to own the vessel through an entity, the interaction between residential ownership structure and yacht ownership structure occasionally creates planning opportunities. These are conversations for counsel, not closing day.

Compare and Contrast: Jupiter Waterfront in Context

The buyers and sellers active in this market are making comparative decisions against other geographies and product types. The following table frames the most common comparison points for buyers evaluating Jupiter against its alternatives.

The comparison most relevant to active buyers in 2025 and 2026 is not Jupiter versus Palm Beach (the two serve different buyer priorities). The more useful comparison is Jupiter waterfront versus other Jupiter products: oceanfront versus Intracoastal versus river basin, and private dock versus marina-first. That decision tree has more practical consequence for daily ownership than any cross-county comparison, and it is best resolved by time on the water.

Bottom Line

Scarcity here is real: by geography, by federal designation, and by policy choices that have held across decades of development pressure. The parcels that front the Intracoastal, the river, and the ocean are in place. New inventory comes from resale, not from raw land. That constraint does not fluctuate with interest rates or development cycles. It is structural. The practical implication is direct: underwrite the parcel before the house. Frontage, depth, bridge geometry, inlet behavior, elevation, and insurance feasibility are the asset. The house depreciates; the quality of the parcel and its water access compounds.

For buyers entering the market: Run the access audit before narrowing geography. Map insurance feasibility, bridge clearances, and inlet behavior by water, not by listing copy. In a market where annual volume never exceeds 142 transactions, the right parcel may surface once. Proof of funds, pre-bind planning, and a marine-aware diligence team should be in place before the search begins, not after the property appears.

For sellers preparing to list: Credibility creates competition. A launch package with current wind-mit, 4-Point, elevation certificate, dock and seawall specs, and preliminary insurance quotes compresses time on market and protects net proceeds. Price to like-kind comps and replacement-cost logic. A price that invites skepticism in a micro-inventory market does not generate counteroffers; it generates silence.

For both sides, the structural point: The 2023-to-2024 correction (30% peak-to-trough, followed by an 18.8% recovery within twelve months) confirmed the asymmetry that defines this corridor. Thin supply limits the accumulation of distressed comparables that extend downturns elsewhere. The market rewards preparation and penalizes hesitation at roughly the same rate.

Transaction statistics reflect MLS closed sales, Jupiter single-family detached residential, Intracoastal / river / ocean / ocean-access canal waterfront only, zip codes 33458 / 33469 / 33477 / 33478, 2016 to 2025. Properties where the sole waterfront classification is lake, pond, interior canal without ocean access, or golf course were excluded. Condos, townhomes, and mobile homes were excluded. Median price and price per square foot figures are derived from this filtered dataset. Days on market figures represent annual averages across closed transactions.

References to buyer behavior, cash share, and discovery cycles reflect practitioner observation across BeachesMLS closed data. These are directional characterizations, not a formal statistical extract. Figures vary by submarket and period and should not be applied to individual property underwriting without direct MLS comp analysis.

This article is a general educational overview. It is not a formal market report and not legal, tax, or investment advice. Equal Housing Opportunity.

Conservation: The Nature Conservancy, Blowing Rocks Preserve (nature.org). National Wild and Scenic Rivers System, Loxahatchee River (rivers.gov).

Access and Nautical: NOAA Nautical Charts, Jupiter and Lake Worth areas (charts.noaa.gov). U.S. Coast Guard, Local Notice to Mariners, District 7 (navcen.uscg.gov).

Insurance: Florida Office of Insurance Regulation, Consumer Resources (floir.com).

Tax: Florida Department of Revenue, Documentary Stamp Tax (floridarevenue.com). Palm Beach County Property Appraiser, Homestead and Portability (pbcgov.org).