The dataset is confined to single-family detached homes at $5 million and above. Condos, townhomes, and sales below $5 million are excluded. Fifteen municipalities are profiled individually; nine are grouped as "Other." What follows is the macro view: total volume, the absorption problem that defines seller strategy, the five-year cycle from frenzy to normalization, and the geographic hierarchy that separates a $2,786/SF island from a $1,065/SF mainland suburb 20 minutes away.

Executive Summary: The Numbers That Matter

Note: MOI based on 590 active listings as of Feb 13, 2026, 33.2 monthly closings as of FY2025. Active inventory was 431 at year-end 2025.

The median-mean divergence ($7.95M vs. $11.03M) reflects the $20M+ segment's outsized influence: 171 sales (~9.7%) contributed ~$5.76B (~29.6%) of total volume. The defining characteristic of this market is segmentation across 24 municipalities, each with its own pricing logic, absorption rate, and buyer profile.

The Absorption Problem

This number deserves its own section because it defines everything else in this report.

In a balanced real estate market, an often-cited rule of thumb is roughly 5 to 7 months of inventory, though that benchmark varies by market segment and price tier. Palm Beach County's $5M+ single-family market has 590 active listings (as of the Feb 13, 2026 data extract) competing for 33.2 monthly transactions (399 closings in 2025 / 12 months): 17.7 months of inventory. That is more than double the upper end of the conventional balanced range. For context, active inventory was approximately 431 at year-end 2025; the jump to 590 reflects seasonal listing activity in early 2026, a pattern consistent with South Florida's spring selling season.

For sellers: At the current run-rate of approximately 33 closings per month, on average fewer than one in 18 active listings will find a buyer in a given month, assuming constant inventory and closing rate. The overwhelming majority of $5M+ listings are competing for a transaction that statistically will not happen to them. Pricing, condition, and presentation are not nice-to-haves; they are the difference between closing and expiring.

For buyers: You have leverage and should use it. With 590 options on the market and roughly 33 transactions closing monthly, patience is rewarded. The 2025 sold-to-list ratio of 92.3% (92 cents on every listed dollar) is a countywide average. Well-informed buyers in specific submarkets are negotiating deeper discounts, particularly on listings with extended days on market.

Why 18 months and not 6: This is not a market in freefall. Supply has structurally outpaced demand at the $5M+ threshold. Many listings are aspirationally priced properties that will either reduce or withdraw. Others are legacy homes requiring significant renovation, properties the market has already told sellers it does not want at the current ask. The figure reflects fragmented demand across two dozen submarkets and every price tier from $5M to $150M, not a uniform glut.

Absorption is decelerating: The trailing 6-month closing rate fell below the full-year average. Seasonality may contribute, but the directional trend warrants monitoring.

The 5-Year Cycle: From Frenzy to Normalization

The period coincided with elevated inbound demand often attributed to tax migration and remote-work flexibility, producing 444 transactions totaling $5.02 billion in 2021 (71-day DOM, 94.6% sold-to-list). In 2022, DOM compressed to 50 days with 95.5% sold-to-list, the seller's apex.

Rate increases trimmed 2023 to $2.68 billion (273 transactions, 89-day DOM, 93.1% sold-to-list). Volume rebounded in 2024 to $3.91 billion with 353 transactions, but sold-to-list held at 92.7%, down 2.8 points from 2022.

2025 delivered $4.71 billion across 399 transactions, the second-highest annual count in this dataset behind only 2021's migration-driven 444. But the 92.3% sold-to-list ratio and 86-day median DOM confirm that more transactions does not mean a tighter market. Buyers are active but selective, patient, and negotiating from a position of strength.

Dollar volumes in billions; $/SF to nearest dollar. 5-year totals: 1,764 sales, $19.46B. Totals reflect unrounded source data. The volume decline from 2021 to 2023 reflects the unwinding of COVID-era migration demand and the impact of rising interest rates on transaction counts, not a decline in per-unit pricing. Median sale price held between $7.55M and $8.20M across all five years.

Median sold price as % of list price. Y-axis truncated (90%–97%) for readability.

The Geographic Hierarchy: Where the Money Flows

347 transactions totaling $5.36 billion. Median sale $11.20 million, $2,786/SF. The island's fixed geography and stringent architectural review sustain pricing power that no other submarket can replicate.

Boca Raton ($3.57B, 403 sales), Jupiter ($2.11B, 211), Delray Beach ($1.37B, 129), and Palm Beach Gardens ($1.15B, 155). Boca at $1,105/SF offers a 60% discount to the Town of Palm Beach. Jupiter at $1,371/SF offers 51% off the island.

Manalapan ($990M, 39 sales) holds the highest median among municipalities in the table at $23.50 million. Gulf Stream's 29-day DOM indicates rapid absorption among closed sales, though its 10.9-month MOI suggests a more nuanced picture.

← scroll →

Bars represent total closed-sale volume. Darker bars = Island/ultra-luxury tier. Values in $B or $M.

This chart reflects only closed sales at $5M and above. Sales below that threshold are excluded entirely, so sub-$5M activity in any municipality does not influence the medians or bubble sizes shown. Manalapan plotted at median $23.5M. The Town of Palm Beach ($11.2M, $2,786/SF) and Gulf Stream ($13M, $2,025/SF) form the premium cluster. Volume markets Boca Raton and Palm Beach Gardens cluster at lower price and $/SF.

The Data Series: Where the Deep Analysis Lives

This report is the overview. The following six reports use the same MLS dataset to answer specific questions about the $5M+ market in granular detail. Each one stands alone; together they form a complete picture.

Bottom Line

Palm Beach County's $5M+ single-family market has structurally repriced from the 2022 peak. The shift is visible in every metric that matters: absorption speed, sold-to-list ratio, and days on market. At 17.7 months of inventory countywide, the structural advantage favors buyers across most submarkets and price tiers, though the repricing is not uniform. Submarkets like Gulf Stream and Tequesta remain tight, while Wellington and West Palm Beach carry years of supply.

For sellers at $5M+: Price to the 2025 sold-to-list curve, not the 2022 memory. Every month on market past 90 days compounds the discount and narrows the buyer pool. Our Speed of Sale report quantifies the penalty by DOM bracket. If your property requires renovation, our What Your Money Buys report shows the construction-era discount you are competing against.

For buyers at $5M+: You are selecting from a pool where fewer than one in 18 active listings transacts each month. Use that ratio. The Geographic Hierarchy above maps which submarkets offer steep $/SF discounts versus the island. Our Seasonal Calendar identifies which quarters historically produce the best buyer outcomes by price tier.

The market's signal: Condition sells, aspiration sits. Submarket selection, construction era, and pricing discipline are the three variables that determine whether a property transacts or expires. The data series above quantifies each one.

Scope: Palm Beach County, Florida. Single-family detached homes only. Closed sales at $5,000,000 or above. Pending, withdrawn, and off-market transactions excluded.

Time Window: January 1, 2021 through December 31, 2025. Inventory as of February 13, 2026.

Data Source: BeachesMLS. Extracted February 13, 2026.

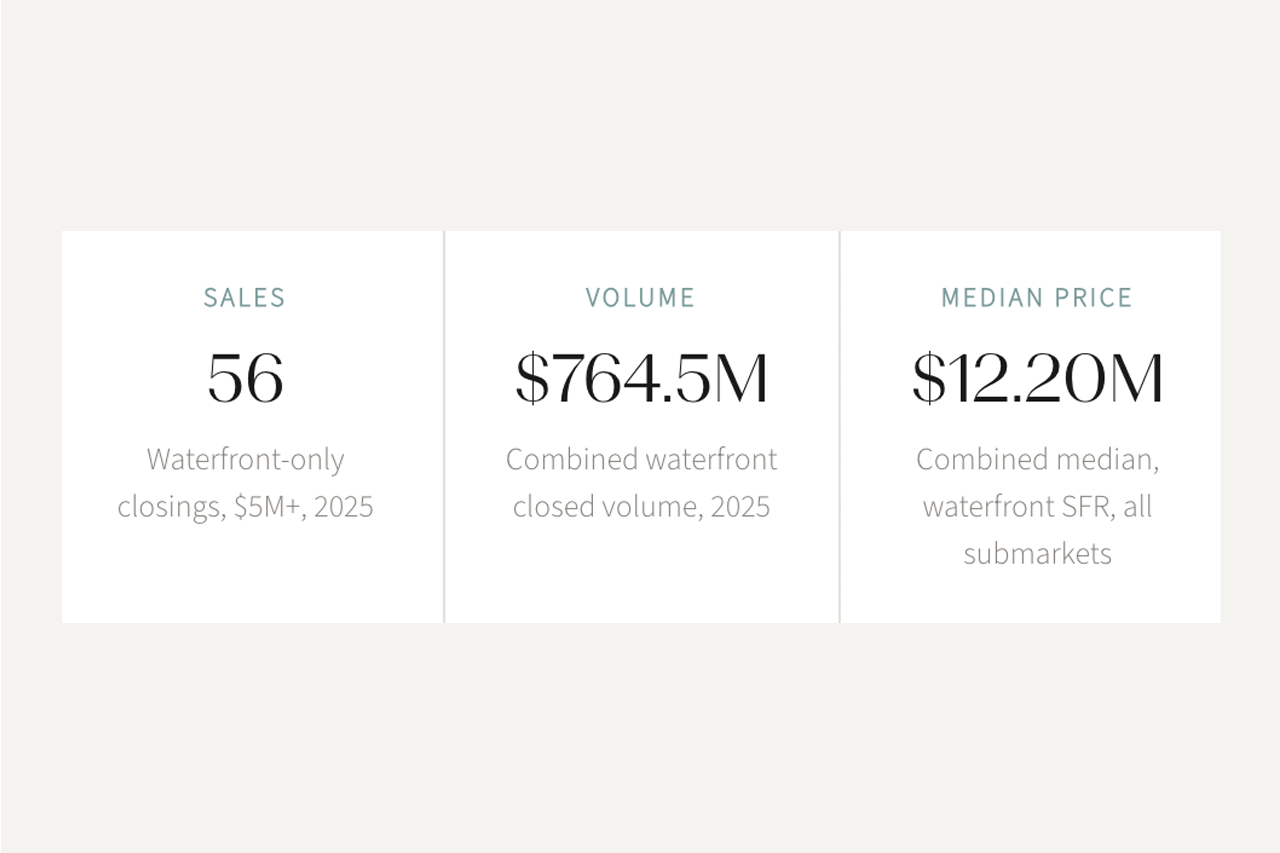

Definitions: "Waterfront" includes ocean, Intracoastal, lake, canal, and river frontage per MLS. "Gated" = communities with controlled access per MLS. "Town of Palm Beach" = incorporated barrier island municipality. "Size" and "$/SF" use the MLS "SqFt - Living" field, which measures enclosed living area and excludes garages, covered patios, and non-living space. "Year Built" and "Construction Era" use the MLS "Year Built" field. "Sold/List" (sold-to-list ratio) = sold price as a percentage of the final list price at the time of sale.

Table Abbreviations: DOM = days on market. MOI = months of inventory. Eff. MOI = effective months of inventory (active listings / trailing 12-month average monthly closings, computed per period). Active = number of active listings as of the data extract date (Feb 13, 2026). Monthly Avg = average monthly closings for the period shown.

Calculations: Months of inventory = active listings / trailing 12-month average monthly closings. Mean = total volume / total transactions. Dollar volumes displayed in billions or millions, rounded to nearest $10M; $/SF to nearest dollar; median and mean prices to nearest $10,000. Two records with invalid days-on-market values (one each in Boca Raton and Palm Beach Gardens) are excluded from all DOM calculations.

Survivorship Bias: DOM, sold-to-list, and $/SF metrics reflect closed transactions only. Properties that were listed but did not sell (active, expired, or withdrawn) are not captured in these figures. In submarkets with low transaction counts, this can overstate market health: fast closings are recorded while slow-moving or unsold inventory is invisible.

Market Data: BeachesMLS closed transaction data, January 2021–December 2025. Active listing inventory as of February 13, 2026. All transaction and pricing figures derived from MLS data as described in Methodology above.